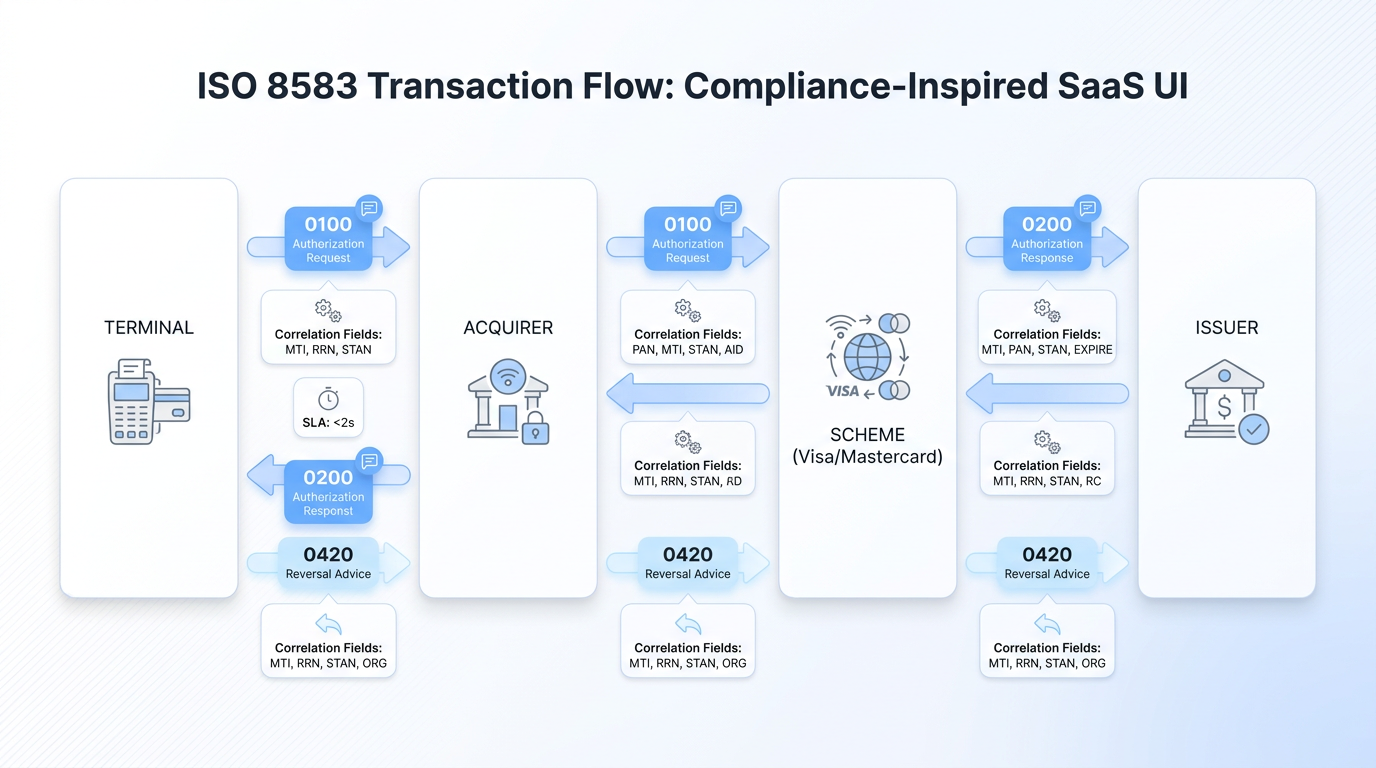

Scheme integration with Visa and Mastercard

Visa and Mastercard both speak ISO 8583, and both speak it differently. Visa's online authorization runs through VisaNet's Single Message System (SMS) and BASE I. Mastercard's online authorization runs through its Authorization Platform, with clearing handled by GCMS over IPM as described in the GCMS Reference Manual: "Every message must contain the message type identifier (MTI) in positions 1-4, followed by both bit maps in positions 5-20, followed by the International Organization for Standardization (ISO)-defined data elements (DE 1-DE 128) in ascending sequence."

In ISO 8583 development, private data elements are where the dialects diverge. Visa uses field 62 for private data with its own subfield catalog. Mastercard uses Private Data Subelements (PDS) inside DE 48 and DE 124. The 3-D Secure cryptogram lives in different subtags. The merchant category code is mandatory on both, but the rules around when to include addendum data differ. None of this is hard once you have read the spec. The hard part is keeping two parallel implementations in sync as both schemes publish quarterly mandates.

Connectivity adds another layer. Mastercard requires connection through a MIP appliance, with Transport Layer Security enhancements rolling out in 2025. Visa terminates connections at its endpoints over leased lines or IPsec tunnels. Both demand a documented disaster recovery posture before they let you go live. Certification is a separate project of its own, and we'll return to it.

Error handling and resilience in ISO 8583 development

Production-grade ISO 8583 development is mostly about what happens when things go wrong. The happy-path code is a few hundred lines. The error-handling code is the rest of the system. In ISO 8583 message processing, response codes in DE 39 are the first signal. 00 is approved. 05 is do not honor. 91 means the issuer was unreachable. 96 is a system malfunction. Each code triggers different behavior on your side, and the rules differ by scheme. A 91 from a Visa authorization is a candidate for retry through STIP. A 96 means something is broken and retries make it worse.

Network management messages in the 08xx range keep the link healthy. The 0800 is a network management request, 0810 the response. These carry echo tests, sign-on, sign-off, key change, and cutover messages. A typical production switch sends an echo test every 30 to 60 seconds on each persistent connection. If three consecutive echoes fail, you mark the link down and fail traffic over to a backup while the on-call gets paged.

The rules for handling malformed input are equally important:

-

Validate the MTI and bitmap before reading any data element. A bad bitmap means everything that follows is suspect.

-

Reject messages with response code 30 (format error) when the wire format is unparseable, rather than guessing.

-

Deduplicate inbound by STAN and RRN within a defined window, because schemes will resend on their own retry logic.

-

Persist every reversal intent before sending it, so a crash mid-send doesn't lose the obligation.

In ISO 8583 development, idempotency is the deepest of these requirements. Two 0100 messages with matching STAN and RRN, plus the same PAN within a short window, are almost certainly the same transaction retried. Your switch needs to recognize that and return the cached response rather than charging the cardholder twice. The same logic applies to reversals in reverse: a duplicate 0400 must result in one logical reversal credit.

Performance and scalability considerations

In ISO 8583 development, the performance budget for an authorization is unforgiving. End-to-end, the cardholder expects a response in under two seconds. Within that envelope, the scheme and issuer use their shares, while your acquiring switch has roughly 100 to 200 milliseconds to do its work. Visa's network alone routes authorizations to the issuer in around 150 milliseconds, and the rest of the budget is consumed by everything outside Visa.

In ISO 8583 message processing, volume compounds the pressure. Mastercard handles "surges of 70,000 transactions a second" during peak periods like the December holiday rush, and Visa's network averages around 8,500 TPS with peaks above 65,000 TPS. Your share of that traffic is a few hundred TPS on a normal day and ten times that on Black Friday. The system has to handle the peak without graceful degradation that affects approval rates.

A few architectural decisions separate switches that scale from switches that crumble:

-

Persistent TCP connections to schemes, with connection pooling on the application side. Reopening sockets per transaction is unworkable at production volume.

-

STAN-based multiplexing on each connection, where many in-flight requests share one socket and STAN correlates each response to its caller.

-

An asynchronous internal model with synchronous external semantics, so internal queue depth absorbs spikes without blocking the network thread.

Observability is the other half. Every message needs structured logging so you can reconstruct a transaction after the fact, but the logs cannot contain raw PANs. PCI DSS Requirement 3.3 requires that you "Mask PAN when displayed (the first six and last four digits are the maximum number of digits you may display)." Requirement 3.4 extends this to logs and backups. The practical answer is to tokenize the PAN at ingress and log only the token plus the first six and last four digits. Structured logs of card transaction messaging that don't respect this rule turn into compliance findings the first time an auditor opens them.

Testing, certification, and going live

Nothing about ISO 8583 development goes live without certification, and certification is its own discipline. The path runs from unit tests against a simulator, to scheme test environments, to a pilot, to general availability.

In ISO 8583 development, simulators come first. Open-source options like jPOS and commercial simulators from vendors let you replay scripted message flows and verify that your parser and builder behave as expected, with the state machine covered by the same scripts. This is where you catch off-by-one bit errors and field length mismatches before they cost you scheme test cycles.

Then comes scheme certification. Visa's Test System and Mastercard's Customer Test Facility run hundreds of scripted scenarios across authorization, reversal, partial approval, currency conversion, and exception handling. Each script has expected response codes and field contents. Miss one and you re-run the entire suite after the fix. Plan for several weeks of test cycles even on a clean implementation.

Production rollout is staged. A pilot with a small slice of traffic, either a single BIN range or a single merchant, runs for a defined period while you watch error rates and latency. Only after the pilot is clean do you ramp to full volume. Shortcuts in this sequence surface later as outages, and outages in card transaction messaging are visible to cardholders, merchants, regulators, and the press.

Wrapping up

ISO 8583 systems outlive the teams that build them. The version of the standard most widely used today was published in 1987, and the switches running it have been patched and extended as they moved across hardware generations without ever being rewritten. Whatever you ship will be in production longer than you expect, and the engineers maintaining it will not have access to the context you carried in your head.

That reality shapes the design. Field-level abstractions that name fields clearly, parsers that are configuration-driven rather than hardcoded, logs that capture every state transition, and reversal logic that is correct under every retry scenario are the investments that pay off over a decade. The protocol is a contract with the wider payments ecosystem.

EGS builds resilient fintech infrastructure for institutions that run card transaction messaging at production scale, and our team works on ISO 8583 message processing and scheme certification, with high-throughput switch architecture part of the same work every day. If you're planning a new ISO 8583 development project or migrating off a legacy switch, reach out to our engineering team for a working session on your architecture; the same session can cover hardening an existing integration before peak season.