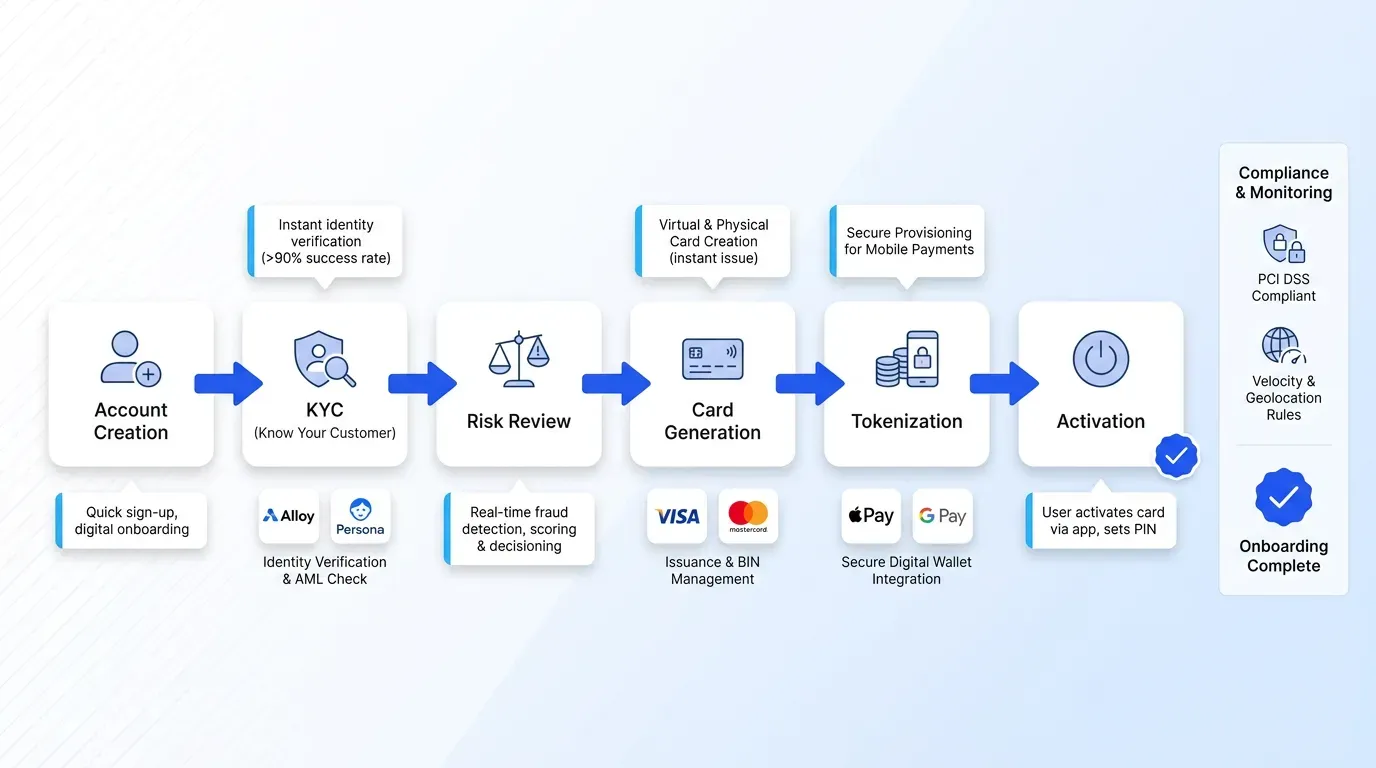

Activation and first use

Activation flips the card status from inactive to active in the authorization system.

The methods depend on the channel:

-

In-app confirmation, where tapping a button in the issuer app activates the card

-

Interactive Voice Response (IVR), where the cardholder calls a number and enters identifying digits

-

First-transaction activation, where the first authorization itself activates the card if it passes risk checks

The first transaction for instant issue debit cards runs through extra velocity and geolocation rules with amount-threshold checks because the card has no behavioral baseline yet. A swipe at the airport thirty seconds after issuance in a different city will get declined, which is the right outcome. Once a clean transaction lands, the activation event closes the loop back to the original account-opening record, and the customer is fully onboarded.

Infrastructure behind real-time card provisioning

Step back from the linear flow and the picture becomes a distributed system that stretches beyond a simple banking workflow. The card management platform is the orchestrator. HSMs handle the cryptography. Network connectivity to Visa and Mastercard runs over leased lines or dedicated VPNs with sub-100-millisecond round trips. Event-driven messaging, such as Kafka or a managed equivalent, carries account-created, card-generated, token-provisioned, and activation events between services that do not share a database.

Two properties matter more than anything else here. APIs have to be low-latency, because users are staring at a loading spinner during onboarding. Operations have to be idempotent, because a retried wallet provisioning call cannot result in two tokens for the same device. Marqeta's product writeup emphasizes Just-in-Time Funding and instant card tokenization as the two features its customers lean on most, and both depend on these properties holding under load. Real-time card provisioning is a systems engineering problem dressed up as a payments problem.

Compliance and security checkpoints

Speed cannot come at the cost of controls, and the controls are non-trivial. The Payment Card Industry Data Security Standard (PCI DSS) governs every system that stores or transmits account data, with processing covered inside the same control boundary. PCI DSS version 4.0.1 was published in June 2024 and tightens requirements around vulnerability management and authentication, with continuous monitoring added to the same control set. The PCI Security Standards Council notes that scope reduction through segmentation can lower assessment cost and reduce risk, which is why most issuers route the PAN through a certified processor rather than touching it directly.

The usual scope-reduction levers in instant issuance design are:

-

Tokenization of the PAN at the earliest possible point, so downstream services handle tokens only

-

Using a PCI Level 1 certified processor for card data storage and authorization

-

Network segmentation between the cardholder data environment and the rest of the bank's infrastructure

-

Client-side encryption for push provisioning payloads, as documented in VGS's integration guide

Network mandates from Visa and Mastercard add their own layer. Fraud monitoring and dispute handling obligations for instant issue debit cards kick in the moment a card is active, and Regulation E in the United States gives consumers liability protections that the issuer has to absorb. Instant card issuance systems that skip these checkpoints don't stay in production long.

Where instant card issuance systems are heading

A few trends are reshaping the pipeline. Pull provisioning is becoming the default in markets where Click to Pay has gained traction, because the card network handles the wallet step on behalf of the issuer. Stablecoin-linked card programs for instant issue debit cards, where a USDC or similar balance funds card authorizations through a Just-in-Time funding hook, are moving from pilot to general availability at processors like Lithic and Marqeta.

AI-driven risk decisioning is compressing the KYC step further. Alloy's pKYC product, launched in 2025, runs continuous compliance monitoring instead of fixed-interval reviews, which lets issuers move borderline applicants out of the manual queue faster. On the supplier side, issuer processors are packaging instant issuance as a turnkey product, complete with BIN sponsorship and wallet SDKs that handle tokenization, so a new fintech can go live in weeks rather than the year or more it used to take.

Key takeaways for issuers and builders

The two delivery models, branch-based and digital-first, share almost the entire pipeline. The hard engineering work sits in tokenization, wallet provisioning, KYC integration, and PCI DSS scope management. Get those four right and the rest of the system mostly takes care of itself. Customer expectations will keep tightening, and the issuers that treat instant issue debit cards as a distributed systems problem will keep winning the onboarding race.

If you're evaluating vendors or building in-house, the question to answer first is which parts of the stack you own and which you rent. EGS builds resilient fintech infrastructure for issuers and processors who need their instant issue debit cards pipeline to stay up under real traffic, with the cryptography and event messaging already in place alongside the compliance scaffolding. Reach out to our team for a working session on your issuance architecture.