What a payment switch actually does

In payment transaction switching systems, a payment switch is the piece of software that sits between acquirers, issuers, card networks, and a bank's internal systems. Its job is to receive a transaction request from one party and pass it on in a form the next party understands after deciding what to do with it. Payment switch development is the discipline of building that middle layer so it stays fast and accurate with the availability production traffic requires.

The switch has three core jobs. First, real-time transaction routing: deciding the downstream path that should receive the transaction. Second, authorization: forwarding the request to the issuer (or standing in for the issuer when needed) and returning an approve or decline. Third, preparing the day's transactions for clearing and settlement so money actually moves between banks.

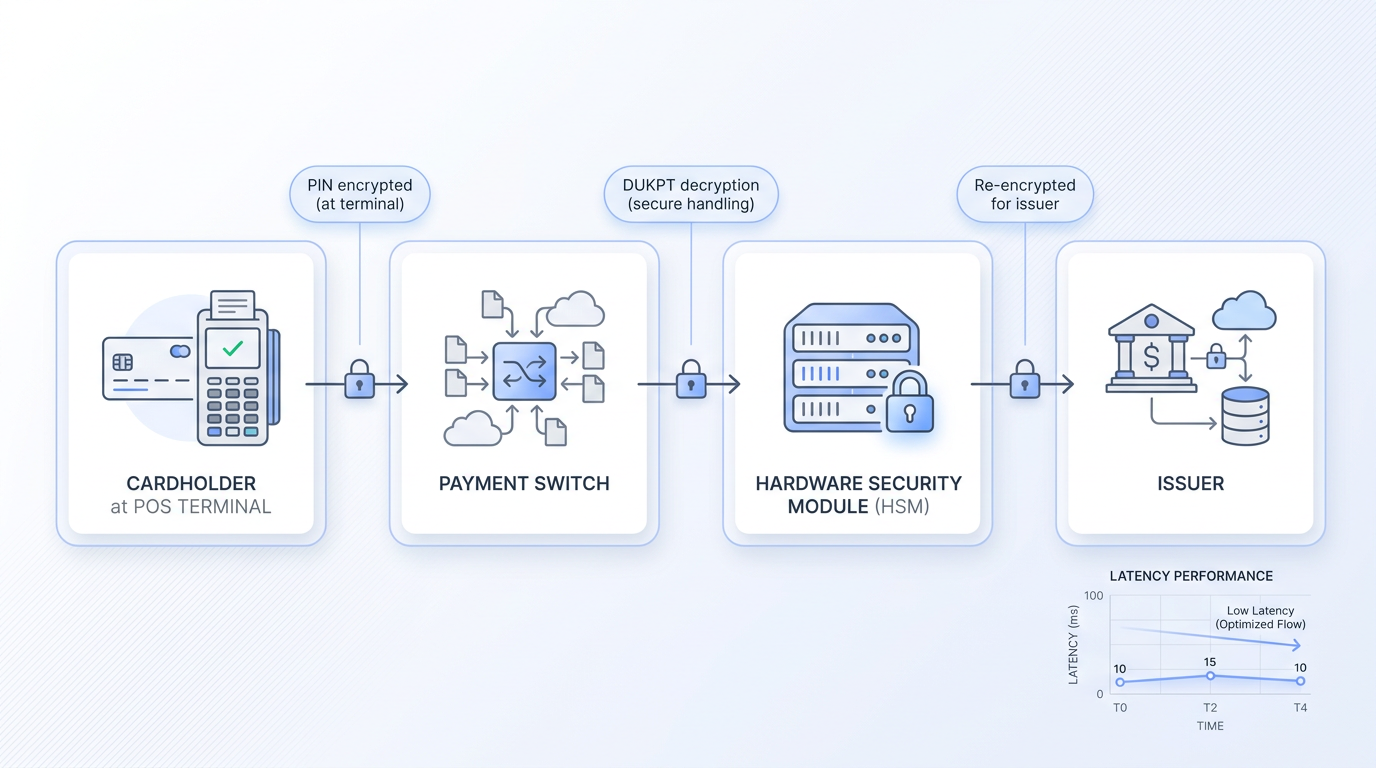

Here is the flow in plain terms. A customer taps a card at a coffee shop. The POS terminal builds an ISO 8583 authorization request and sends it to the acquirer. The acquirer's switch uses the card's Bank Identification Number (BIN) to identify Visa and route the message to the Visa network. Visa forwards it to the issuing bank's switch, which checks the balance and applies fraud rules before it replies with response code "00" for approved or "05" for declined. The response retraces the path back to the terminal. The entire round trip finishes in under two seconds.

Why the switch is the core engine

Every transaction in payment transaction switching systems passes through the switch. The mobile app, the POS, the e-commerce checkout, the core banking ledger, they all sit on one side or the other of it. That position is what makes the switch the real engine of payment processing, because every design decision inside it shows up in the customer's experience.

Latency is the clearest example. If the switch adds 200 milliseconds to each hop because of synchronous database calls or chatty logging, that delay reaches the terminal and the cardholder feels it. Reliability in payment switch development works the same way. When the switch drops a connection to the scheme, the front-end app has nothing useful to show. Cost per transaction also lives here, because real-time transaction routing choices made inside the switch determine which acquirer fees apply.

Front-end teams get the credit for a smooth checkout, but the switch is doing the work that makes the checkout possible. That is why banks and processors that take payments seriously invest in payment switch development as a long-term engineering capability.

Core capabilities of payment switch development

A switch that handles production traffic has to do several things well at the same time. The capabilities below are the ones that decide whether the platform holds up on Black Friday or falls over at 11 a.m. on a Tuesday.

Real-time transaction routing

Real-time transaction routing is how the switch decides where each message goes. The decision draws on the card's BIN range, the scheme (Visa, Mastercard, local network), the currency, the merchant category, the acquirer's contractual rules, and the cost of each available path. All of this happens in single-digit milliseconds because the customer is already waiting.

Most switches structure this as a combination of fast lookup tables for BIN and scheme data plus a rule engine for the business logic. Least-cost routing picks the cheapest acquirer that can settle a given transaction, which matters because interchange and scheme fees eat directly into margin. Fallback paths matter just as much. If the primary acquirer times out, the switch needs to retry through a secondary route without double-charging the cardholder.

When real-time transaction routing is done poorly, you see the symptoms in production: approval rates drop because traffic keeps hitting a degraded acquirer, and fees climb because the cheapest path is never selected.

Authorization and clearing flows

Payment transaction switching systems participate across the full lifecycle from the authorization request to the later clearing process, with capture handled along the way. Authorization is the real-time check that the funds and the card are good, signaled by a 0100 request and 0110 response in ISO 8583 terms. Capture happens when the merchant confirms the sale at end of day. Clearing is the batch process that produces the files banks exchange to actually move money.

Stand-in processing in payment switch development is the part that earns the switch its reputation. When the issuer is unreachable because of a network failure or maintenance window, the switch can approve low-risk transactions on the issuer's behalf using pre-agreed limits and a stored risk profile. The transaction completes, and the issuer reconciles later when it comes back online after the cardholder walks away with their coffee.

Reconciliation files tie all of this together. At cutoff, the switch produces settlement files that match every authorized transaction to its capture and clearing record. If these files do not balance, the operations team spends the next morning chasing breaks instead of working on anything productive.