Regulations that shape the architecture

The three pillars turn legal obligations into architecture. They're what the law requires, translated into engineering. Every design decision in the sections above maps to a specific obligation you already answer to, which is why enterprise IAM security in a bank is inseparable from compliance.

Start with the Sarbanes-Oxley Act. Under sections 302, 404, and 409, login activity and information access must be monitored and logged with an audit trail covering all access to sensitive financial data. That's the traceability pillar written as statute. The Gramm-Leach-Bliley Act adds the Safeguards Rule, which under 16 CFR 314.4 requires financial institutions to enforce enterprise IAM security through role-based access controls and multi-factor authentication, with audit logging across every system holding nonpublic personal information. And PCI DSS governs the identity layer directly through Requirements 7 and 8: Requirement 7 restricts cardholder data access to documented business need, while Requirement 8 mandates a unique ID per user and bans shared or generic accounts.

Where identity meets compliance

Compliance requirements across SOX, GLBA, and PCI DSS look different on paper, but they create the same architectural challenge: proving that the right people have the right access at the right time. Strong financial identity systems translate these regulatory requirements into enforceable controls rather than treating compliance as a manual review process.

A few obligations recur across all three regimes, and financial identity systems have to satisfy each one by design:

-

Segregation of duties, so no single person holds conflicting permissions, which SOX section 404 treats as a core control.

-

Least-privilege access, which gives each user the minimum rights their job requires and sits at the center of PCI DSS Requirement 7.

-

Regular access certification, with PCI DSS 4.0 requiring a review of access to remedy inappropriate permissions, effective March 2025.

Automatic access logging cuts across everything, and PCI DSS 4.0.1 requires audit logs to be retained for a minimum of 12 months, with three months immediately available. Read these mandates back against the pillars and the connection is direct. Traceability is SOX and GLBA logging. Least privilege and segregation of duties are how you pass a PCI DSS access review. The architecture is driven by regulation, and a design that ignores one breaks the other.

Build, buy, or partner

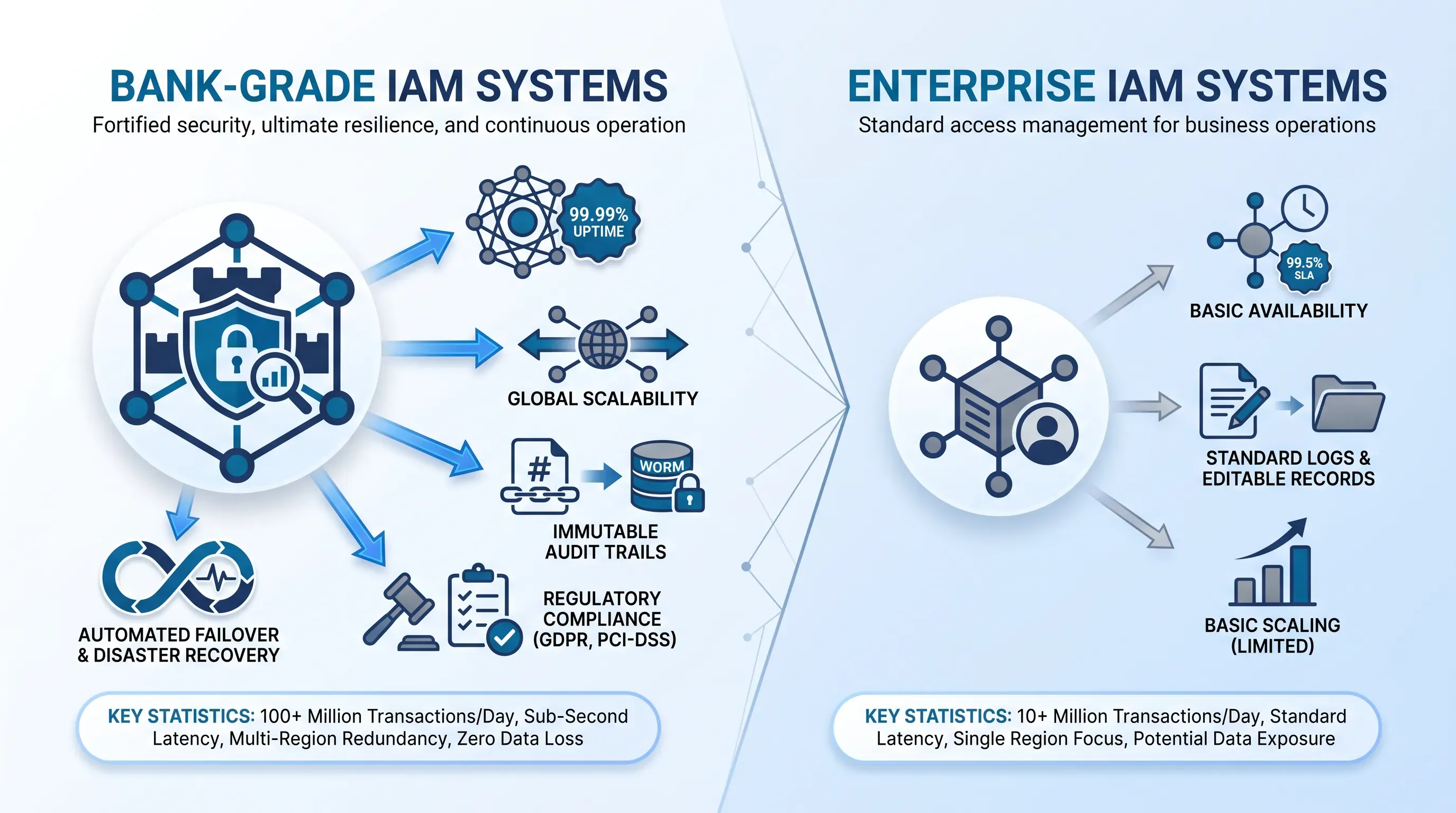

So the real decision is which path gets you bank-grade IAM systems that clear all three pillars and every regulation tied to them. Each option carries a different risk, and the one you pick is a choice you'll defend to a board and a regulator.

Building in-house gives you full control and a perfect fit to your integrations. The trap is that teams underestimate exactly the properties that define the tier. High availability with automated cross-region failover and tamper-resistant audit logging are hard to build and harder to retrofit, especially when horizontal scale has to hold at peak. The TSB failure was an in-house migration where inadequate testing met production load, and the bill ran into hundreds of millions. Buying an off-the-shelf platform solves scale and uptime, since vendors like Okta and Ping have proven both, but generic products don't always fit a specific regulatory posture or a legacy integration a bank carries from an acquisition. Ping, for instance, is built for hybrid and legacy complexity that Okta handles only through added modules, which tells you how much the fit varies.

Choosing a bank-grade identity solution

Partnering with a specialist to build a compliant system sits between the two. You get financial identity systems designed to your requirements without carrying the full risk of a from-scratch build.

Whichever path you weigh, hold it against a short set of criteria drawn from everything above:

-

Does it deliver four-nines availability with automated failover across regions, or does it degrade to a partial-HA default?

-

Will it hold at your real peak user volume without a later redesign?

-

Are audit logs complete and tamper-resistant, with queries available on demand, and do enterprise IAM security controls map to the applicable regulations?

If an option can't answer all three cleanly, it isn't bank-grade, whatever the sales deck claims.

Build your IAM system with EGS

That's the gap EGS is built to close. We design bank-grade IAM systems with availability and auditability treated as first-class requirements from day one, and we set scale before the architecture is locked. The pillars this article defends are the ones we engineer against, and the regulations that shape them are the obligations we design to meet.

A specialist build partner gives you the regulatory fit an off-the-shelf product misses and the depth an in-house team underestimates on high availability and audit traceability. If you're assessing that choice for your platform, our team can talk through what truly bank-grade IAM systems require for your specific volume and compliance obligations, with integrations in scope.