Issuing infrastructure you actually need

A card issuing program is an integrated system. The pieces have to share data cleanly and fail predictably, with recovery that does not lose transactions.

The core components of any serious issuing infrastructure:

-

Issuer processor that handles scheme connectivity, authorization, and clearing

-

Card management system for lifecycle events, status changes, and reissuance

-

Ledger that records every cardholder balance and movement with audit-grade accuracy

-

Fraud and risk engine running real-time scoring on authorization messages

-

Dispute and chargeback tooling aligned to scheme timelines

-

Reporting stack for regulators, schemes, finance, and product teams

Feature lists sell well in sales decks. They don't determine whether a program scales. API quality and uptime do, with observability behind both. A processor that publishes a 99.99% Service Level Agreement (SLA) and exposes p95 and p99 latency by endpoint is doing something different from one that ships a glossy portal and a quarterly status email. When a card declines at a grocery checkout, the cardholder doesn't care that the dashboard has dark mode.

The issuing infrastructure also has to absorb the security overhead. Payment HSMs, key ceremonies, PCI DSS audits, and PCI Card Production requirements bind every component that touches a PAN. Cutting corners here is how programs lose their certifications and their sponsor banks in the same quarter.

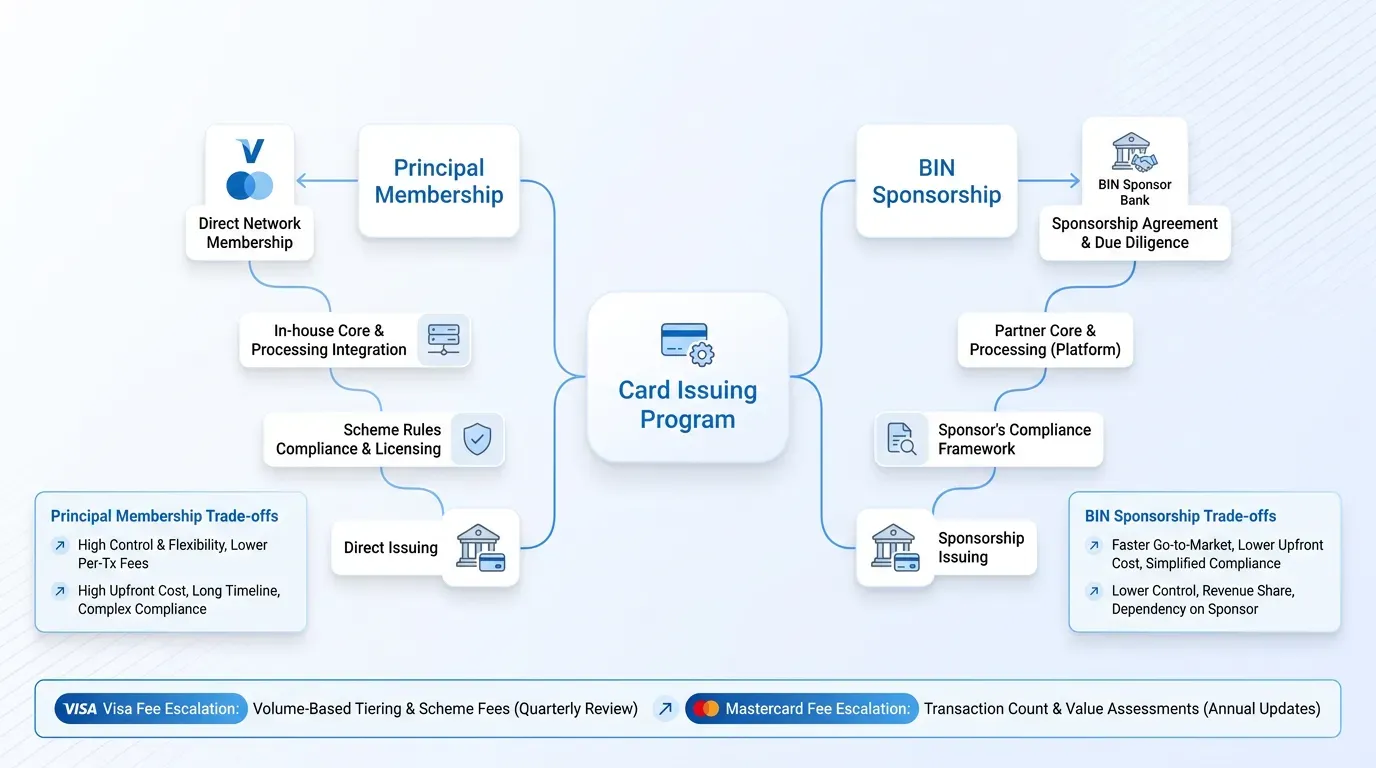

Build, buy, or partner for card program management

Every team launching a program faces the same fork. The choice is whether to build the issuing infrastructure in-house or rely on outside providers, from point solutions to a full-stack partner that owns processing and scheme connectivity along with compliance.

Building card issuing infrastructure yourself makes sense if you have bank-scale volume and a deep engineering bench, with a roadmap that depends on owning every layer. The cost is years of work before you write your first authorization. The classic mid-market approach has been to assemble best-of-breed point solutions, a processor here, a KYC vendor there, a fraud engine bolted on, a card management system underneath. It works, but integration becomes the product. Alex Johnson of Fintech Takes argues that teams choosing this path should focus on providers that enable competitive differentiation and save money on the commoditized layers.

A partner model collapses the integration burden. You get a single contract for processing, scheme connectivity, compliance support, and tooling, in exchange for less control over individual components. For most fintechs launching their first card product, partner-led card program management is the pragmatic path because it shifts the regulatory and engineering load off the product team. Building still wins when scale and unit economics justify owning the stack end to end.

Scaling a program without breaking it

A program with 50,000 cards looks nothing like one with 5 million. Volume spikes during paydays and holidays test the issuer processor. Multi-currency settlement adds reconciliation complexity. Expansion into a new region brings a new license and a fresh set of scheme certifications, along with a new sponsor. According to the Nilson Report's 2024 figures, global card fraud losses reached $33.41 billion in 2024, and fraud patterns shift faster than rule-based engines can keep up.

Three pressure points show up first as programs grow:

-

Authorization latency under load, which directly drives decline rates and merchant abandonment

-

Dispute volumes, where a 0.1% chargeback ratio turns into thousands of cases a month and a full operations team

-

Reconciliation drift between authorization, clearing, settlement, and the ledger, which compounds into reportable breaks

Scale exposes the foundations laid on day one. A processor that runs fine at 100 transactions per second can fail at 10,000. A ledger that batched reconciliation overnight can't survive multi-region settlement windows. The infrastructure choices made before the first card is issued either enable the next million cards or block them.

How EGS supports issuers behind the scenes

EGS provides the resilient fintech infrastructure for card program management that sits behind a card program, so the team running the product can rely on it instead of building it. That includes the issuer processor, scheme connectivity, ledger and reconciliation, fraud and dispute tooling, and the compliance support that comes with operating in regulated markets. The work that consumes most of an engineering and compliance team is the work EGS absorbs.

For a fintech or neobank, and for an embedded finance platform, this means the product team owns the cardholder experience and growth strategy while it also sets the proposition; the heavy operational and regulatory load runs on infrastructure built for it. The same issuing infrastructure architecture that supports a 10,000-card pilot keeps working when the program hits a few million cards in multiple currencies.

If you're planning a new card issuing program or rebuilding one that's outgrown its current setup, talk to the EGS team. We'll walk through your target markets and scheme requirements, then show you what card issuing looks like when the backend is someone else's problem, with timelines included in the plan.