Why chip payments are hard to build

You can build software. You've just been handed EMV POS software as a project, and the first thing you've discovered is that accepting a chip card has almost nothing in common with reading a magstripe swipe. A swipe hands you a block of static data and asks you to send it onward. A chip card negotiates.

An EMV transaction is a back-and-forth conversation between the card and the terminal. When the transaction goes online, the issuer's host joins, and cryptography underpins the exchange. The card authenticates itself. The terminal runs risk checks. The card decides, cryptographically, whether it wants to go online or settle on the spot. None of that happens in a magstripe world, and each piece has to be implemented correctly or the transaction breaks in ways that are hard to diagnose.

Underestimating this is the single most common reason payment projects slip past their deadlines. Teams scope EMV POS software as if it were a data-forwarding job and then hit the certification wall months later. The point here is to give you the real shape of the work so you can scope it honestly, then decide whether to grow this expertise in-house or bring in help.

How an EMV transaction flows

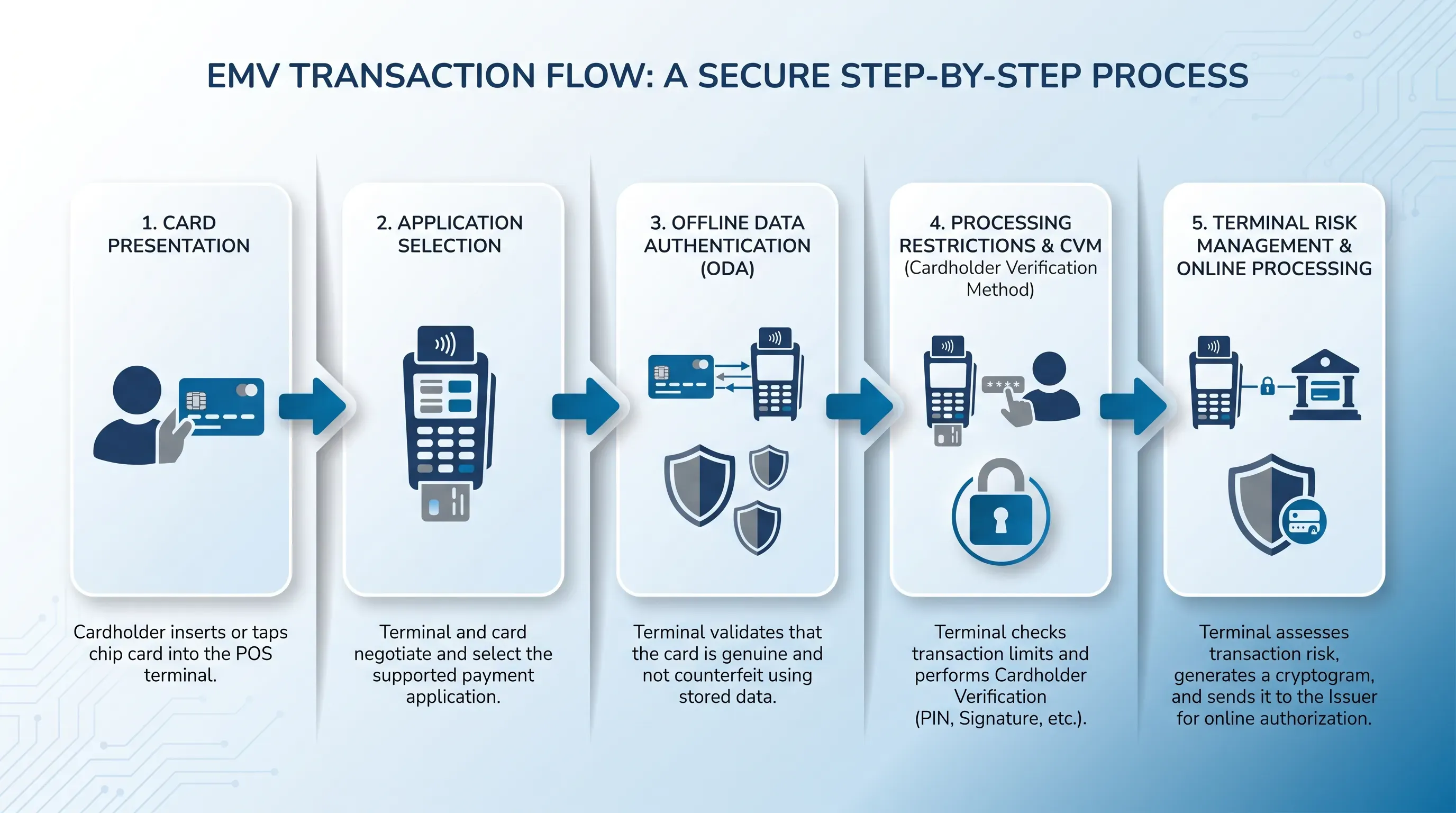

An EMV transaction is a sequence of stages, and each one exists to close a specific gap that magstripe left open. Trace the whole path once and the architecture of your EMV POS software starts to make sense. What follows is the flow an engineer would see if they could watch the messages move between card and terminal.

Card insertion and app selection

The moment a cardholder presents a card, the terminal has to figure out what it's talking to. With a chip, the reader and the card first agree on which payment application to run, because a single physical card can carry more than one. For example, one card holds both a scheme-branded credit application and a common debit application, and the terminal has to pick the right one.

The mechanism behind this is application selection. On contact, the reader asks the card for a directory of what it supports and builds a candidate list of applications the card and terminal both recognize before it chooses by priority. On contactless, the reader queries the Proximity Payment System Environment (PPSE) instead, and the card returns each application's identifier with a priority indicator so the reader can select automatically.

Contact and contactless entry points behave differently here, and that difference matters later when you test. Contact selection can involve cardholder choice between applications, while contactless is built to resolve without asking. Get the entry-point logic wrong and the terminal either picks the wrong application or fails to start the transaction at all.

Chip card processing and authentication

Once an application is selected, the terminal's EMV POS software reads the card's data records and moves to card authentication, the step that confirms the card is genuine rather than a counterfeit clone. This is the heart of chip card processing, and it's where the fraud problem magstripe couldn't solve gets addressed directly.

Authentication splits into two ideas. Offline Data Authentication (ODA) is a cryptographic check the terminal performs locally, without contacting the issuer, to validate that the card's data hasn't been altered and that the card holds a legitimate key. According to B2 Payment Solutions, there are three ODA methods. Static Data Authentication (SDA) checks a signature over static card data. Dynamic Data Authentication (DDA) has the card generate a unique signature for each transaction, while Combined Data Authentication (CDA) signs the transaction data along with the card. American Express now mandates DDA for new card issuers because SDA can't catch a card that copied all the original data. Online authentication, by contrast, happens when the issuer's host validates a cryptogram in real time.

Cardholder verification runs alongside this. The card and terminal agree on a Cardholder Verification Method (CVM), which is how the person is confirmed to be the legitimate cardholder. Common methods include an offline PIN checked by the chip and an online PIN sent to the issuer. With a phone, on-device verification confirms identity with a fingerprint or passcode. The reason this whole chip card processing block exists is fraud prevention. If authentication is implemented wrong, counterfeit cards that should have been caught here sail straight through.