The global migration timeline

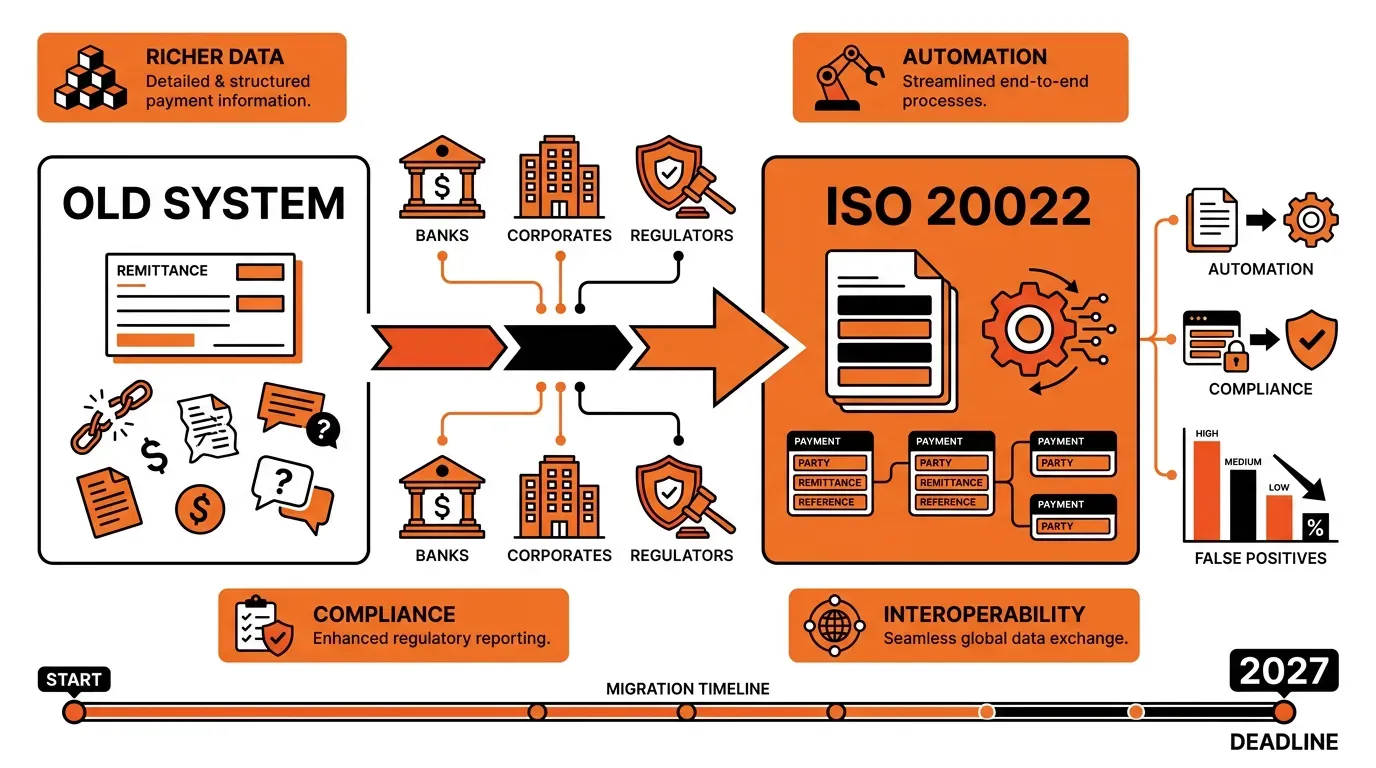

The ISO 20022 migration has been a phased global program. The big milestones are easy to track once you know where to look.

The Eurosystem went first among the major hubs. On 20 March 2023, T2 replaced TARGET2 as the real-time gross settlement system for the euro area, with EBA Clearing's EURO1 cutting over the same weekend. SWIFT began its cross-border coexistence period on the same date through CBPR+, so MT and ISO 20022 messages could flow side by side.

The UK followed quickly. On 19 June 2023, CHAPS and the Bank of England's Real Time Gross Settlement System migrated. The United States took longer. Fedwire originally planned a March 2025 cutover, but the Federal Reserve pushed the date to 14 July 2025, when the legacy Fedwire Application Interface Manual (FAIM) format was retired in a single-day implementation with no coexistence phase.

The big one for cross-border traffic was 22 November 2025, when SWIFT ended the MT/ISO 20022 coexistence period. Key MT messages such as MT103 and MT202 were retired as the mandatory format for payment instructions across the SWIFT network, which connects more than 11,000 financial institutions worldwide. SWIFT has left a narrow fallback window until November 2026 with additional validations and charges, but the message is clear: the ISO 20022 payment system is now the default for cross-border traffic. In Asia-Pacific, schemes like Japan's Zengin and Australia's New Payments Platform adopted the standard earlier, while several markets continue their own ISO 20022 migration on regional timelines.

Challenges banks and businesses face

The benefits are real, but the work behind them is heavy. Legacy core banking systems were not designed for XML payloads or structured addresses, and rewriting them is expensive. Many banks have responded by bolting translation layers in front of older platforms, which gets them compliant without fixing the underlying data model.

That approach has limits. SAP Fioneer cited a survey finding that 48% of U.S. financial institutions plan to implement only the minimum requirements for Fedwire and SWIFT, with no broader modernisation plans. The risk is that the rich data that justified the whole exercise gets stripped on the way into a legacy ledger, so the bank ships ISO 20022 messages but doesn't gain the operational benefit.

The practical headaches show up in several places:

-

Data truncation when MX messages get mapped to internal MT-shaped tables, with the industry convention of appending a "+" character to signal dropped data.

-

Vendor coordination across core banking, payment hubs, screening engines, and reporting tools, each on its own release cycle.

-

Staff training, because operations teams who spent twenty years reading MT tags now have to think in XML schemas and structured address rules.

Smaller institutions and corporates feel the pressure more sharply than tier-one banks. A community bank that relies on a correspondent for cross-border payments still has to understand what's changing, because the ISO 20022 payment system changes customer-facing fields and the statement layouts that feed reconciliation files. The cost of getting it wrong is paid in failed payments and unhappy clients.

How to prepare for adoption

Preparation starts with a data audit. Map every payment field your systems produce and consume, then compare them against the ISO 20022 message types you'll actually exchange. The goal is to identify where information will be lost or misrouted, including cases where duplicate data would create production issues.

From there, the work follows a familiar path. In a note on the Bank of England's CHAPS approach, Akhil Rao noted that the UK rollout sequenced enhanced data requirements over years; purpose codes and LEIs were introduced gradually before they became mandatory. That phased pattern is worth copying.

A grounded preparation plan covers a few priorities. Run a gap analysis against the message types your business depends on; start with pacs.008, pacs.009, pain.001, and camt.053. Select payment service providers and SWIFT-accredited partners whose roadmaps match your modernisation strategy rather than fighting it. Build a test plan that exercises edge cases such as structured addresses and long remittance strings, with exception flows like camt.056 cancellations included in the same plan. Train operations and compliance staff on the new field names and codes before go-live, not after.

The ISO 20022 migration also gives finance and treasury teams a reason to revisit reconciliation processes. If your accounts receivable system can finally consume structured invoice references end-to-end, that's an automation project waiting to happen. The modern payment messaging standard rewards organisations that treat the transition as a chance to redesign workflows.

What comes next

The ISO 20022 migration is the beginning of a longer arc. The same modern payment messaging standard that now carries cross-border wires is the foundation for instant payments and request-for-payment flows, with open banking relying on the same data layer. As central bank digital currencies move from pilots to production, they'll need a messaging substrate that supports rich identity and purpose data, which is exactly what ISO 20022 already offers.

The next wave will focus on what banks do with the data. Centralised payment data stores and canonical data models are where the strategic value sits, especially when analytics use structured payment flows. Maharaja Subramanian of Volante Technologies described the Fedwire cutover as a moment to accelerate broader payment transformation, and that framing applies to every institution that has now crossed the line.

The ISO 20022 payment system is now the working layer of global finance, and assessing your readiness against it is no longer optional. If your team is mapping out the next phase of your ISO 20022 migration, treat this as the start of a multi-year investment in the modern payment messaging standard and the products it will support. Reach out to our payments team to review your current architecture against the ISO 20022 payment system roadmap and identify where data quality and automation can improve customer experience next.