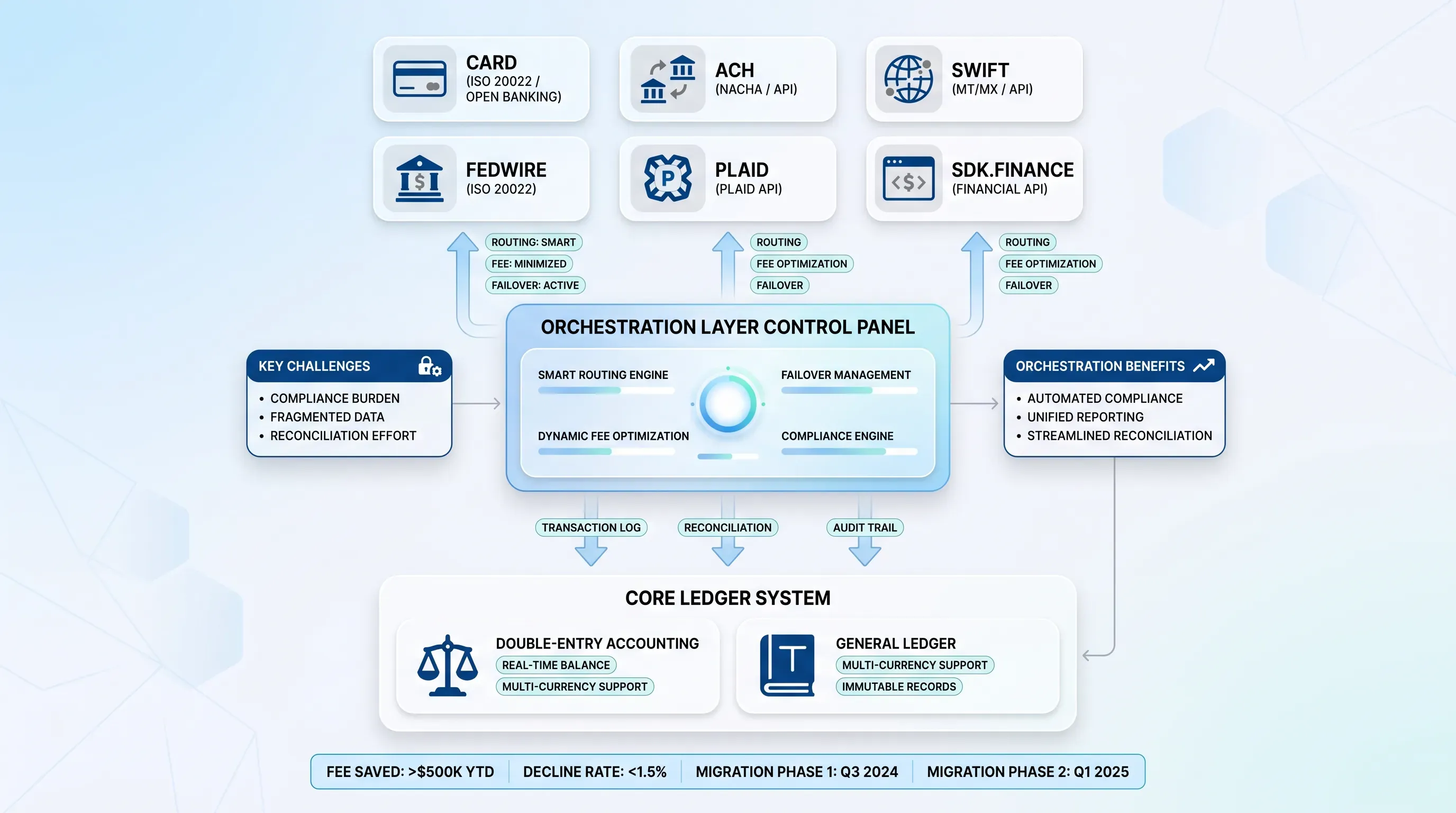

Settlement and reconciliation per rail

Once money moves, the work isn't over. Each rail settles and reports on its own clock and in its own format, and the orchestration layer has to pull all of that back into one view. Cards settle on a batch cycle. A SEPA transfer lands next business day. SEPA Instant confirms in seconds. Each one drops its data into a different account with a different reference structure.

The messaging standards differ too. Card systems have long run on ISO 8583, while bank and instant rails are moving to ISO 20022. That migration is well underway: the Federal Reserve completed its Fedwire migration to ISO 20022 in July 2025, and SWIFT retired legacy MT payment messages in November 2025. Supporting both formats at once is now table stakes for anyone running mixed rails.

Leave this unsolved and your finance team has to match data by hand across several dashboards as it tracks why one rail's total doesn't tie out to the ledger. The fix is a double-entry ledger as the single system of record. Every rail event maps to one consistent set of statuses, so the ledger stays the operational truth while the general ledger handles reporting. As one SDK.finance guide notes, the transactional ledger acts as the source of operational truth while the general ledger feeds compliance and reporting. Storing a running balance in a single field instead invites drift you can't audit.

Keeping money consistent across rails

This is the deepest problem in multi-rail payments, and it's the one in-house teams underestimate most. The core difficulty in multi-rail wallet development is that every rail defines finality differently. Cards stay reversible through chargebacks for months. Bank transfers can remain conditional or recallable for days, and a SEPA Direct Debit carries an eight-week unconditional refund right. SEPA Instant, by contrast, is irrevocable the second it clears.

Now put those clocks inside cross-rail wallet systems. A payment that looks final on an instant rail can be undone by a refund or chargeback on a card rail that funded the same balance. If your system treats "received" as "cleared" without accounting for each rail's reversal window, you've built a false sense of settled money into your ledger.

Why a unified ledger matters

The consequences are concrete. A marketplace that credits a seller's wallet the instant a card payment posts, then lets that seller cash out over SEPA Instant, has created real exposure. If the card payment charges back weeks later, the funds are already gone and irrecoverable. That's liquidity risk and a fraud vector rolled into one, and it comes straight from mismatched finality rather than any single bug.

Consistency, then, is a state-management and ledger problem. Three things solve it together. Idempotency makes sure a retried or duplicated request produces one financial outcome instead of two. Visa's network reported a 92% reduction in duplicate transactions after tightening idempotency controls, which shows how much silent double-processing hides in systems without it. A unified state model maps every rail's own statuses to one shared vocabulary, so "pending" means the same thing whether it came from a card or an instant transfer. And the ledger stays the source of truth at all times, so funds remain in the right state until the relevant reversal window has actually closed.

Build in-house or bring in a specialist

Everything above leads to one decision: build this yourself or work with a team that already has. Be honest about what in-house multi-rail wallet development demands. Multi-rail wallet development means months of specialized engineering before the first transaction clears. Each rail needs its own certification, and those certifications don't stay done. Compliance monitoring runs continuously, and the operational discipline to keep the ledger consistent as you add rails is a permanent commitment after launch.

The alternative is working alongside a team that has already solved routing and cross-rail consistency. That team has also run fee optimization and per-rail settlement under real volume. That experience is what de-risks the project, because a seasoned partner has already hit and fixed the failure modes described earlier, from the false-final balance to the duplicate charge. Manual reconciliation is part of that same pattern.

So the real question is where your engineers' time earns the most. If your edge is your product and your market, spending a year rebuilding payment plumbing that already exists is a strategic cost.

Talk through your rail mix

The right rail mix and orchestration design depend on your markets and volumes. Your payout logic and regulatory footprint shape the same decision. There's no single correct architecture, which is exactly what a short conversation can clarify for your specific situation.

EGS has handled multi-rail wallet development and operated multi-rail wallet infrastructure, and can help you avoid the costly missteps this article laid out, from mismatched finality to reconciliation drift. Book a call with our team to talk through your multi-rail payments roadmap and where multi-rail wallet development fits your plans.