Benefits for issuers and users

For issuers, digital card issuance changes the economics and the relationship. A card that activates in seconds means a cardholder starts spending sooner, which lifts early engagement and revenue. Skipping the plastic for a digital-first card cuts manufacturing and postage costs outright. And because the card lives inside the issuer's app during push provisioning, the issuer keeps a direct channel to the customer at that moment.

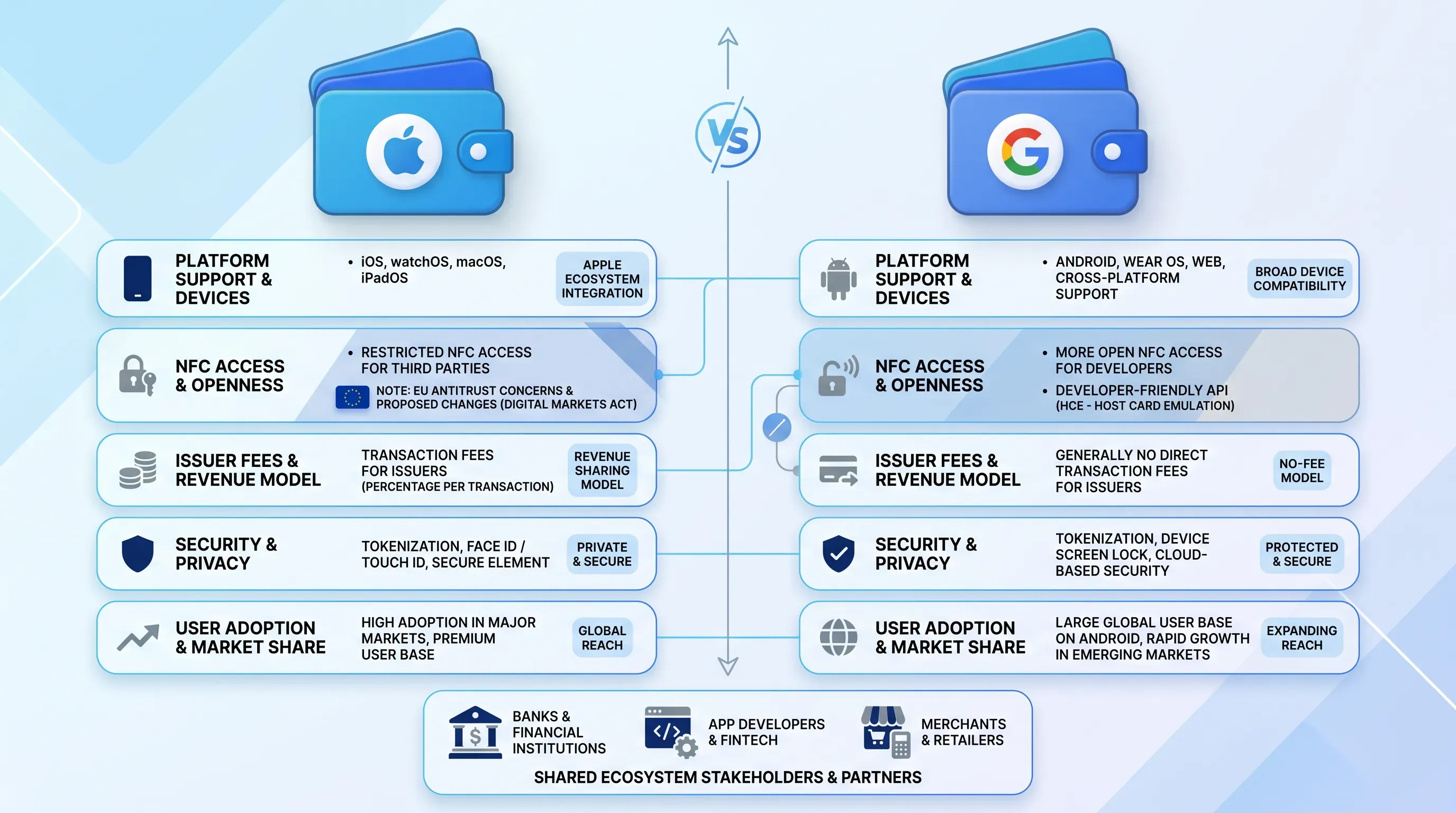

For users, the appeal is immediate access and a stronger sense of safety. Someone approved for a card can pay before lunch instead of waiting a week for the mail. The token model means a stolen phone doesn't hand over a working card number, and biometric checks like Face ID add another lock. Apple Pay alone reached an estimated 744 million users globally in 2024, up from 507 million in 2020, which shows how comfortable people have grown with paying by phone.

These gains feed the broader move toward instant payments. ACI Worldwide's trend report shows that mobile wallet payments rose 105% from 2019 to 2024, and adoption is now strong across every generation. When digital card issuance puts a card into a wallet for tap-to-pay in one sitting, the wait that defined card delivery for decades disappears.

Common challenges to watch

Provisioning isn't friction-free, and the first hurdle is verification. If the identity check fails or stalls, the card never makes it into the wallet and the cardholder gives up. Issuers reduce this by tuning their risk paths carefully, so genuine customers sail through a green path while only riskier sessions get pushed to a yellow-path second factor.

Fraud during enrollment is the sharper threat. The US Payments Forum names mobile wallet provisioning fraud as a primary form of account takeover, where a fraudster tries to load a stolen card onto their own device. The defense is a layered one: strong authentication at enrollment and real-time scoring of each provisioning attempt, with token revocation the instant a card is canceled. A relaxed checkpoint at provisioning is exactly where attackers look for a way in.

The last hurdle is inconsistency across devices and regions. A wallet feature that works on one platform behaves differently or is missing entirely in another market, and supported card networks vary by country. Issuers smooth this out by testing across both major wallets before launch and by setting clear expectations about where mobile wallet integration is available. Getting these pieces right is what separates a clean rollout from a stream of support tickets.

Where digital payments go next

The direction is steady and clear. Physical cards keep losing ground as wallets become the default, and the data backs it up. Digital tap-to-pay volume is projected to grow over 150% by 2028, with wallets on track to become the default alternative payment method at US point of sale by 2027, per Chargeflow. New use cases keep arriving too, from transit and digital ID to buy-now-pay-later options layered on top of the wallet.

For issuers, the question is how well their provisioning experience holds up. A smooth path into Apple Pay and Google Pay, backed by solid fraud controls, is becoming table stakes. If you issue cards, this is the moment to review how digital card issuance and mobile wallet integration perform across the platforms your customers actually use.

EGS builds resilient fintech infrastructure that supports digital card issuance and mobile wallet integration so issuers can move cards into wallets securely and at scale. To evaluate your own provisioning strategy or see how this fits your card program, reach out to our team for a consultation.