How to route and retry

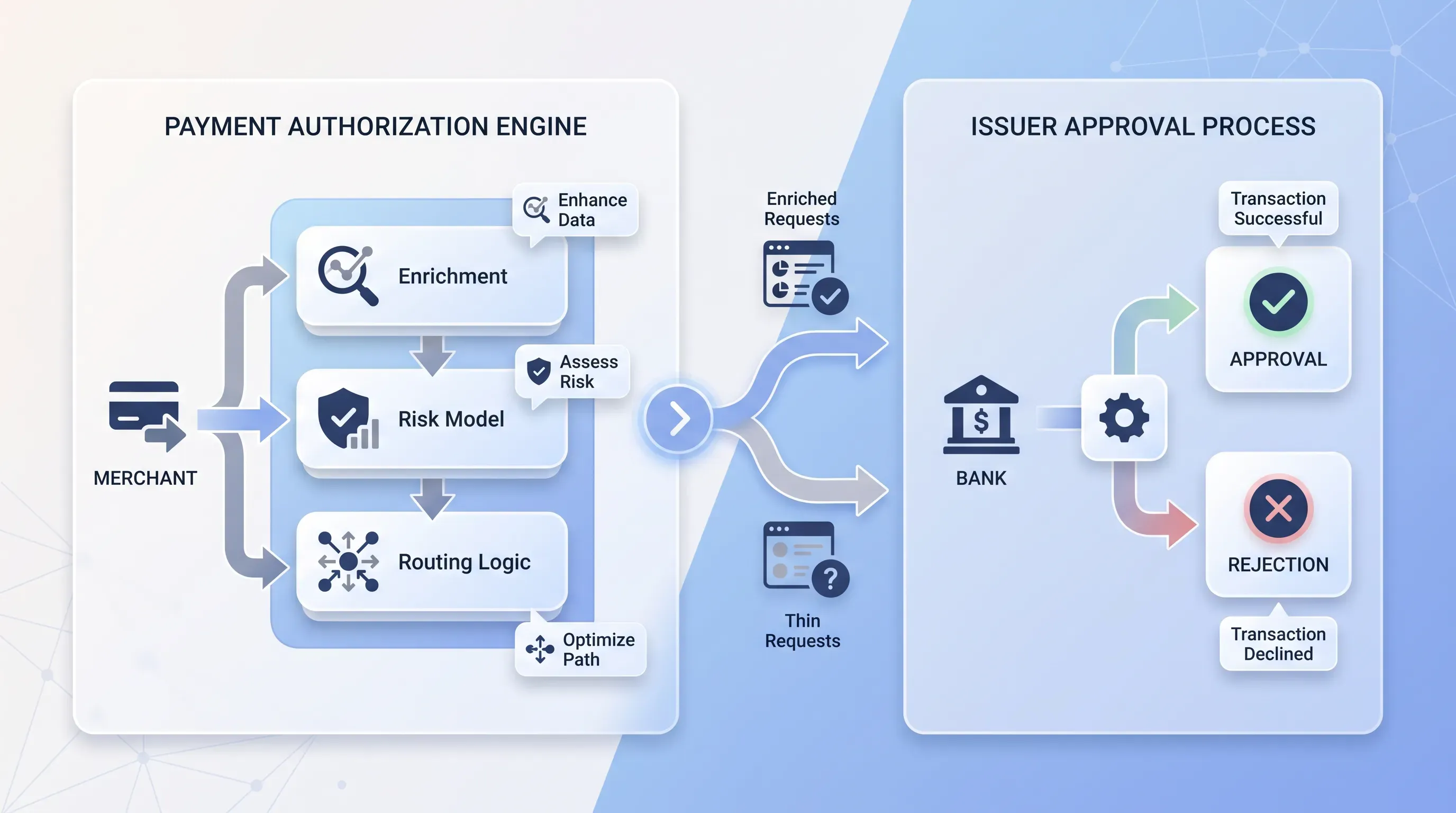

The third decision is the path and the second chance. Smart routing sends each transaction down the acquirer most likely to approve it, based on the issuer relationship and how that card's BIN range maps to geography. The gains are concrete. Solidgate reports that Zeely combined acquirer migration with routing and cascading for a +8pp approval rate lift, with risk metrics down 40% in three months.

Retry logic is where teams hurt themselves most. The discipline is telling a soft decline from a hard one. Soft declines account for 70 to 90% of card-not-present failures, things like insufficient funds or an issuer timeout, and they're worth another attempt. Hard declines, like a stolen card or closed account, are permanent. Retry the wrong ones and you irritate issuers, trigger scheme fines that damage your standing. Retry the right ones with proper timing, and published recovery rates run from 30% to 70% of soft-declined transactions. Orchestration is what makes routing and cascading possible in the first place, since it gives the engine more than one path to try.

Lifting approvals without adding risk

Here's the tension the article has been building toward. The same payment authorization engine that raises approvals can raise fraud and operational drag if you tune it carelessly. The goal is to win approvals without trading away control.

The good news is that these aren't opposing goals as often as people fear. Filtering junk before authorization lifts approval rates and cuts fraud in the same move, because cleaner traffic earns issuer trust while bad attempts never land. Network tokenization does the same double duty. And applying authentication selectively, rather than challenging every shopper, holds conversion while shifting liability on the transactions that warrant it.

The operational side matters as much as the fraud side. Manual review is expensive and slow; it costs an average of $3.47 per transaction according to Signifyd, and as many as 23% of e-commerce orders were manually reviewed in 2025 per MRC data. When the engine makes cleaner decisions on more transactions, fewer orders sit stuck in a queue, and your team stops doing low-value triage. That's how the engine reduces drag while it lifts revenue.

Tradeoffs and what to watch

None of this is free, and pretending otherwise would do you no favors.

The honest costs are worth naming before you commit:

-

Migration and integration take real effort, especially if you're moving from a single-provider setup to a coordinated one.

-

More moving parts mean more architectural complexity to monitor and reason about.

-

Over-tuned rules block good customers, and the cost shows up months later in retention data that rarely gets traced back to the fraud layer.

Approval rate is a metric you watch continuously, because issuer behavior and your own traffic mix shift underneath you. A setup tuned last year drifts. The decision to build versus buy changes the math here. Building an authorization or payment orchestration layer in-house gives you control but loads the ongoing maintenance onto your team, while buying shifts the per-acquirer complexity to a provider at the cost of some flexibility. Neither answer is universal, and the right call depends on your volume and how much of this you want to own.

Where to start

Start by measuring what you have. Pull your current credit card authorization rate, then look at where declines cluster by issuer, geography, and card type. Those patterns reveal where revenue is leaking. From there, review your payment authorization engine's decisioning logic and identify which controls you actively manage versus which still rely on default settings.

A focused audit often uncovers quick wins, whether that's network tokenization, intelligent retry strategies, or routing optimizations. The key is treating payments as a revenue growth lever rather than a back-office function.

At EGS, we help merchants identify hidden authorization losses and implement strategies that increase approval rates without increasing acquisition spend. Our payment experts work with businesses to optimize authorization performance, reduce unnecessary declines, and recover revenue that would otherwise be lost.

If you'd like to understand where your authorization rates can improve, book a call with the EGS team for a tailored assessment of your payment setup.