Compliance built into the architecture

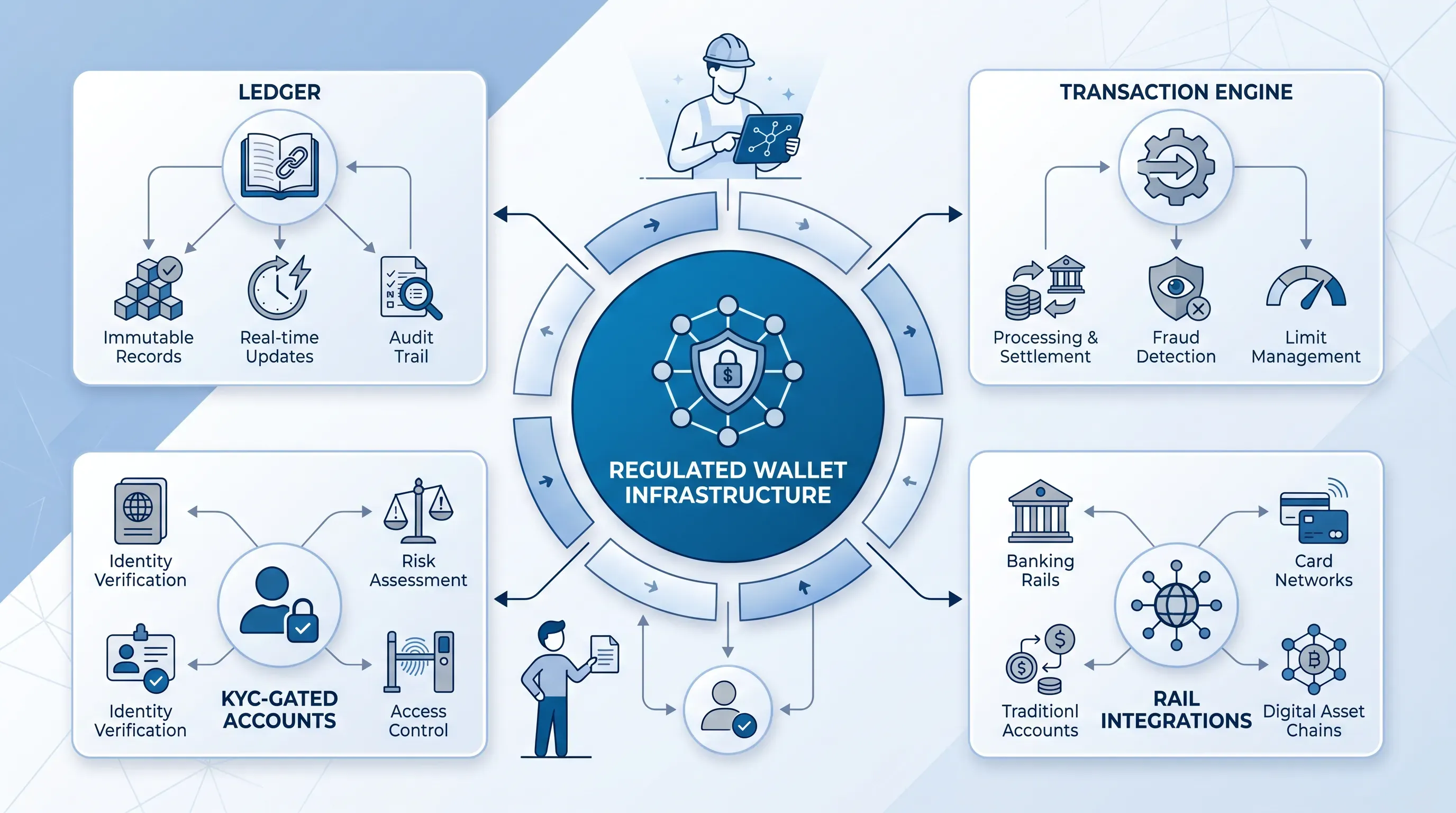

In regulated wallet infrastructure, fintech wallet architecture treats compliance as a set of design constraints built into the system before launch. The obligations reach into onboarding and transaction monitoring from the first commit, and data-handling requirements shape concrete ledger decisions while also affecting the engine and accounts.

Start with anti-money-laundering (AML monitoring) and screening. Rule-based systems are notorious for noise, with 90% to 95% of alerts turning out to be false positives per long-cited PwC analysis, and manual review running $25 to $50 per alert at mid-size institutions. That cost lands directly on your architecture, because the monitoring layer needs clean, structured movement data from the transaction engine to segment risk and cut the false-positive load rather than drown analysts.

Building compliance into the payment lifecycle

Then there is the Payment Services Directive 2 (PSD2), with its strong customer authentication rules, and the framework moving toward PSD3. The European Commission proposed PSD3 and the Payment Services Regulation in June 2024, and Adyen notes a final version expected in Q1 or Q2 of 2026. Authentication is a state the transaction engine enforces before a movement posts, which means SCA logic lives inside the lifecycle.

Safeguarding is where the previous section and this one meet. Under the UK's new rules, effective from 7 May 2026, payment and e-money firms must run internal and external safeguarding reconciliations at least once each reconciliation day and segregate client money from operational funds. Daily balance-level reconciliation is a safeguarding control the regulator now expects to see, which ties compliance-by-design straight back to the reconciliation architecture described above. KYC gating closes the loop, because segregated, traceable funds start with a verified identity attached to every account.

Scaling and auditability challenges

What breaks as a wallet running on regulated wallet infrastructure grows from thousands to millions of transactions is rarely the happy path. Balance drift compounds, and exception queues outpace the humans who review them once rail-specific settlement quirks become a swarm at volume. On top of that sits the audit trail, which has to survive a regulatory examination years after the movements it records.

So treat auditability as a first-class design goal, on par with throughput. Every movement must be reconstructable and every balance defensible in a compliance review, which is only possible when the ledger is immutable and event-sourced from the start. Compliant wallet systems that manage this were built for it. The ones that treated reconciliation and audit trails as cleanup, to be added once the product found traction, end up firefighting under regulatory pressure with no clean history to fall back on.

The Synapse failure is the cautionary version of this contrast. Reports showed that its ledgers were inaccurate and did not record how much customers held, while pooled funds across a network of banks made it impossible to determine who was owed what. The lesson for anyone deciding how much foundational rigor to buy before volume arrives is that audit and reconciliation are cheap to design in and brutally expensive to retrofit once real money is moving through the system.

Building financial grade wallet infrastructure with EGS

A financial-grade wallet built on regulated wallet infrastructure comes down to an accurate ledger and reconciliation built as architecture, with compliance and audit-ready scale designed in from day one. None of them retrofit cleanly once transactions are flowing and an examiner is asking questions.

EGS builds compliant wallet systems and has solved these problems before, so your team does not have to learn them through production incidents. That covers the decisions that quietly sink projects, from double-entry ledger design and per-rail reconciliation tolerances to safeguarding controls and swappable rail adapters that let you add SEPA or FedNow without a rewrite. The result is fintech wallet architecture that stays defensible as volume climbs.

If you are building or replatforming a wallet that holds and moves real money, book a call with EGS to talk through your specific design and where regulated wallet infrastructure de-risks the work ahead.