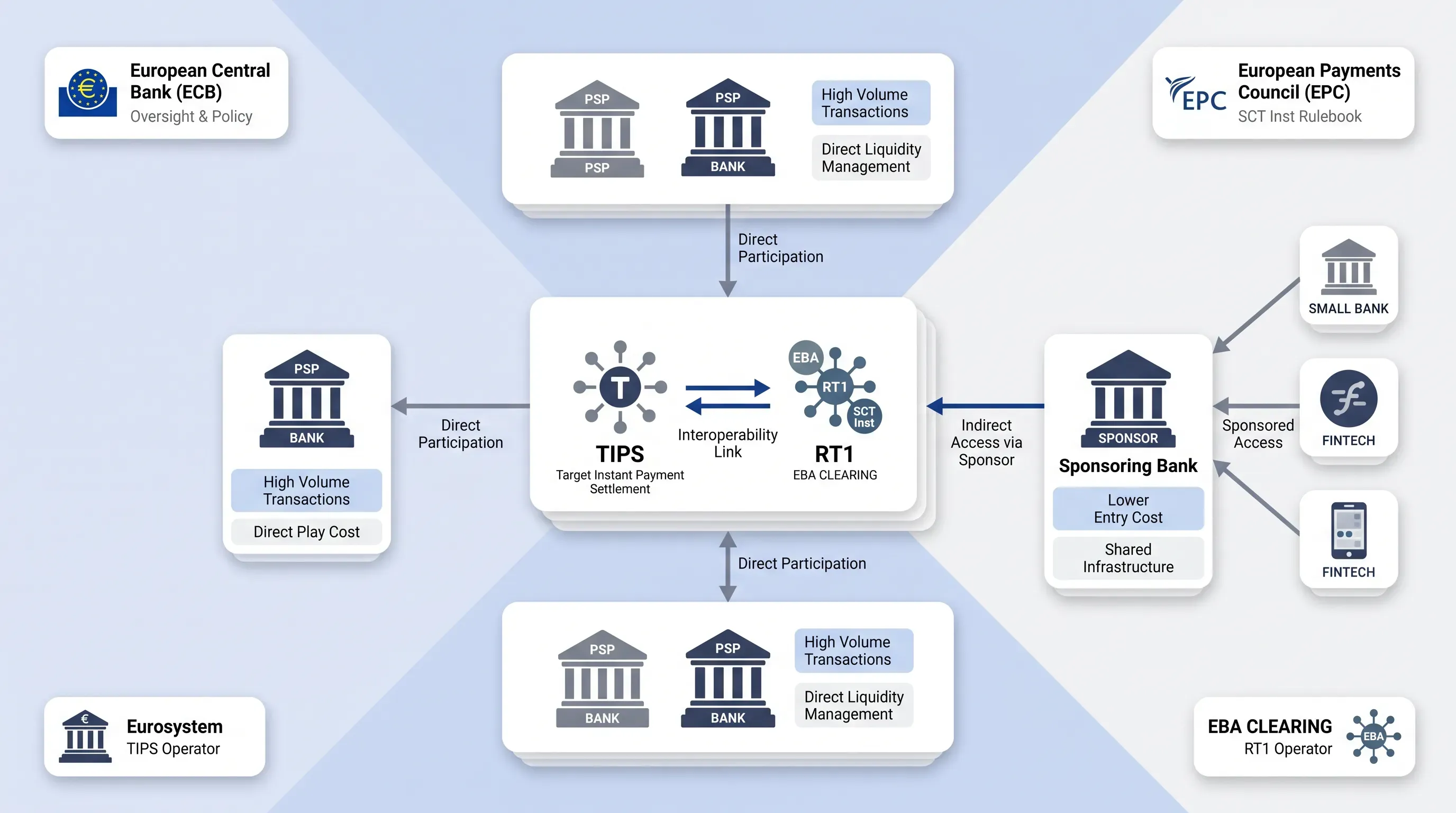

Who runs the SEPA Instant infrastructure

The chain has a handful of distinct roles, and your first job is to find where you sit. Map them, and the participation decision in front of you becomes much clearer.

The payment touches these parties:

-

Originating PSP: the payer's bank, which validates the transfer and sends it after screening.

-

Beneficiary PSP: the payee's bank, which credits the account and returns the confirmation.

-

Clearing and Settlement Mechanisms for SCT Inst systems: TIPS, run by the ECB, and RT1, run by EBA Clearing, which route messages and settle the cash.

-

The central bank: the Eurosystem holds the settlement accounts and provides the central bank money that makes TIPS settlement risk-free.

-

The European Payments Council: the scheme owner that writes and maintains the SCT Inst rulebook.

Not every institution connects to TIPS or RT1 directly. There is a difference between direct and reachable-via-intermediary participation, and it's the core decision you'll face. A TIPS participant holds its own DCA and settles on its own account. A reachable party accesses a participant's account under a contractual agreement, while an instructing party submits payments on behalf of others. A smaller bank or a fintech without direct central-bank access can reach the SEPA Instant infrastructure rails through a sponsoring bank that holds the settlement account and processes on its behalf.

That sponsorship route is the realistic path for most fintechs. You still adhere to the SCT Inst scheme and meet the screening and verification rules while you lean on a participant for the settlement leg. The scale of the network is already large. As of November 2024, the EPC counted 2,627 SCT Inst scheme participants, about 73 percent of all SCT adherents across SEPA and 85 percent within the euro area.

What the EU regulation requires

The Instant Payments Regulation (IPR) was adopted on 13 March 2024 and amends the existing SEPA Regulation. It turns instant euro transfers from an option into a duty for any PSP that already offers standard euro credit transfers. The obligations arrive in a defined order, and the dates differ by participant location.

The sequence runs receive first, then send. Euro-area banks handling SEPA instant payments had to be able to receive instant payments by 9 January 2025 and to send them by 9 October 2025. Non-euro-area member states get longer, with receiving due by 9 January 2027 and sending by 9 July 2027. Electronic money institutions and payment institutions follow their own track, with most obligations landing in 2027. Price parity sits alongside these: the fee for an instant transfer cannot exceed the fee for a standard one, and for euro-area banks that rule applied from 9 January 2025.

The regulation also rewrites the validation step we traced earlier. Two obligations matter most:

-

Verification of Payee (VoP): before the payer authorises a transfer, the PSP checks whether the payee's name matches the IBAN and returns a result that ranges from a match to no match, with close match as an intermediate outcome. The VoP scheme took effect on 9 October 2025 for SEPA PSPs offering SCT or SCT Inst, and the check must be offered at no extra charge.

-

Sanctions screening: PSPs now run daily checks on their own customers, which keeps the ten-second window clear of slow list lookups.

The stakes for missing these dates are not trivial. Penalties under the legislation reach up to 10 percent of a bank's turnover, which is why the screening and VoP work belongs near the top of your project plan.

Planning your SEPA Instant infrastructure connection

You now have enough to scope the work. The decisions ahead are concrete: choose direct participation with your own settlement account or access to SEPA Instant infrastructure through a sponsoring bank, then decide whether the technical connection is built in-house or bought while treasury prepares liquidity and prefunding for a system that settles at every hour. Add the VoP and screening capabilities the regulation demands, and bring the technical and control teams into the room early, because the deadlines have already started passing and the rails reward institutions that prepare ahead of them.

EGS builds resilient fintech infrastructure for institutions connecting to these rails, from sponsored access through to the screening and verification layers the regulation now requires. If you're scoping a SEPA Instant infrastructure project, reach out to our team to map your options against the deadlines.