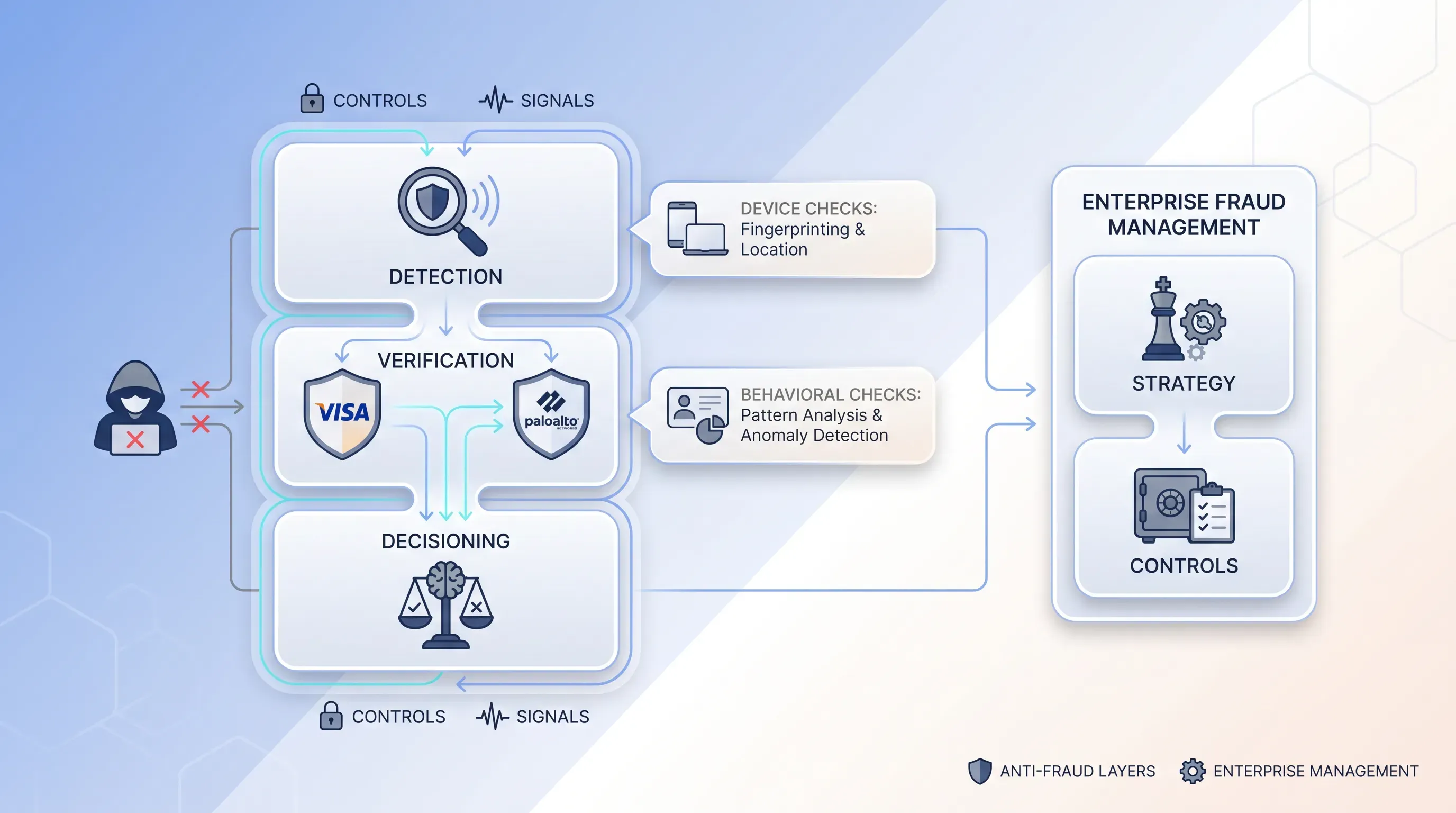

Decisioning and orchestration

All of this produces scattered signals, with an identity outcome from onboarding and a device score from fingerprinting. The decisioning or orchestration engine is what turns them into one verdict. It ingests every signal and applies rules and models that decide in milliseconds whether to allow the action or escalate it through a challenge or a block. Ping Identity describes the risk decision engine as the central hub that aggregates signals like login behavior and device fingerprinting to spot suspicious activity that standalone tools would miss.

This is the connective tissue that makes the whole thing an anti-fraud architecture instead of a toolbox. Cleaner, deduplicated identity signals feed better rules and sharper models, and Sardine notes that a stable fingerprint layer reduces noise from fragmented journeys and improves the inputs that fraud models depend on. Feed the engine fragmented data and it makes fragmented decisions. Feed it one coherent view and the decisions get sharper with every session.

Orchestration is also where your team keeps control. SAS describes its decisioning platform letting teams combine business rules with anomaly detection and machine learning, and tune strategies through champion-challenger testing. That means you set the risk appetite. The engine enforces it consistently across every channel.

How the layers work together

The claim worth proving is that the layers are stronger connected than summed. Walk through an account takeover to see why. An attacker buys a stolen credential and logs into a customer's banking account. The credential is valid, so a login check alone waves them through. But the browser fingerprinting layer doesn't recognize the device, and the WebGL hash is new. None of those signals is damning on its own. Together they raise the session's risk score.

That score is what triggers the next move. In the IC3's account takeover playbook, the attacker now needs the one-time passcode, so they pose as a bank employee and ask the victim for the code. Even if the OTP is surrendered, the decisioning engine has already combined the device and IP anomalies with a new-payee request into a single elevated verdict. It calls a step-up: a document or biometric identity verification check the attacker can't pass. The layers caught what each alone would have missed.

Why connected signals catch what point solutions miss

Now run a synthetic onboarding attempt. A fabricated identity, real Social Security number stitched to a fake name, clears a basic data check at signup. The identity verification layer flags weak document corroboration but isn't certain, so the account opens under watch.

Then browser fingerprinting does the work the snapshot couldn't:

-

The same device fingerprint appears behind eleven other recent applications.

-

An antidetect browser is detected attempting to vary each profile.

-

The sessions share network signals that link them as one operation.

The decisioning engine ties the weak onboarding signal to the device-ring pattern and blocks the cluster before any of the accounts can bust out. The value lives in the handoffs. The onboarding doubt and the device-ring evidence meant nothing apart, and everything together.

Building your anti-fraud architecture

You don't need a rip-and-replace project to move from a patchwork to a connected stack. Start by mapping what you already own onto the layered model. Put each existing control in its place: the signup identity check is your onboarding layer, and the rules engine is the start of your decisioning layer. Laying the tools against the model this way makes the gaps obvious.

Then find what's uncovered and sequence the fixes. A practical order looks like this:

-

Map every current control to a layer and note which journey moments have no coverage.

-

Close the widest gap first, with continuous device signals between onboarding and step-up, since that's the blind spot fraud rings exploit.

-

Wire the layers into shared decisioning so signals stop dying inside individual tools.

The harder part is organizational. Fraud and risk each own a different piece of this, with security and architecture pulled into the same product decisions, and they have to agree on shared signals and who owns the decisioning layer. Without that agreement you rebuild the silos in software. Get the teams aligned on one decisioning fabric and the model holds.

Watch for two common pitfalls. One is over-reliance on a single layer, where identity verification becomes the whole defense even though it's a point-in-time snapshot that synthetic identities are built to pass. The other is letting friction creep into low-risk flows, which quietly drives away good customers. SEON points out that failed payments contribute to nearly half of all customer churn, so every needless challenge in a safe flow has a cost. The model exists to put friction where the risk is and nowhere else.

Where EGS fits in

The layered model of anti-fraud architecture only helps if you can buy and deploy the pieces. EGS's digital fraud and identity solutions map onto this architecture as concrete components. The identity verification capability covers onboarding and step-up moments, since it confirms a real, eligible person before they transact and returns to the front when risk justifies a harder check. The device-level signals from browser fingerprinting fill the long gaps in between, as they watch every session quietly and feed the decisioning layer that turns scattered signals into one verdict.

Adopting these as part of one connected stack lets you close the specific gaps you found when you mapped your current controls, without stitching together unrelated vendors whose tools never learn from each other. The layers share signals by design, so each decision is sharper than the sum of its inputs.

If you've mapped your stack against this model and can see where the coverage thins, that's the place to start. Line your current controls up against the layers described here, and talk to EGS about the layers you're missing so your anti-fraud architecture works as one connected defense.