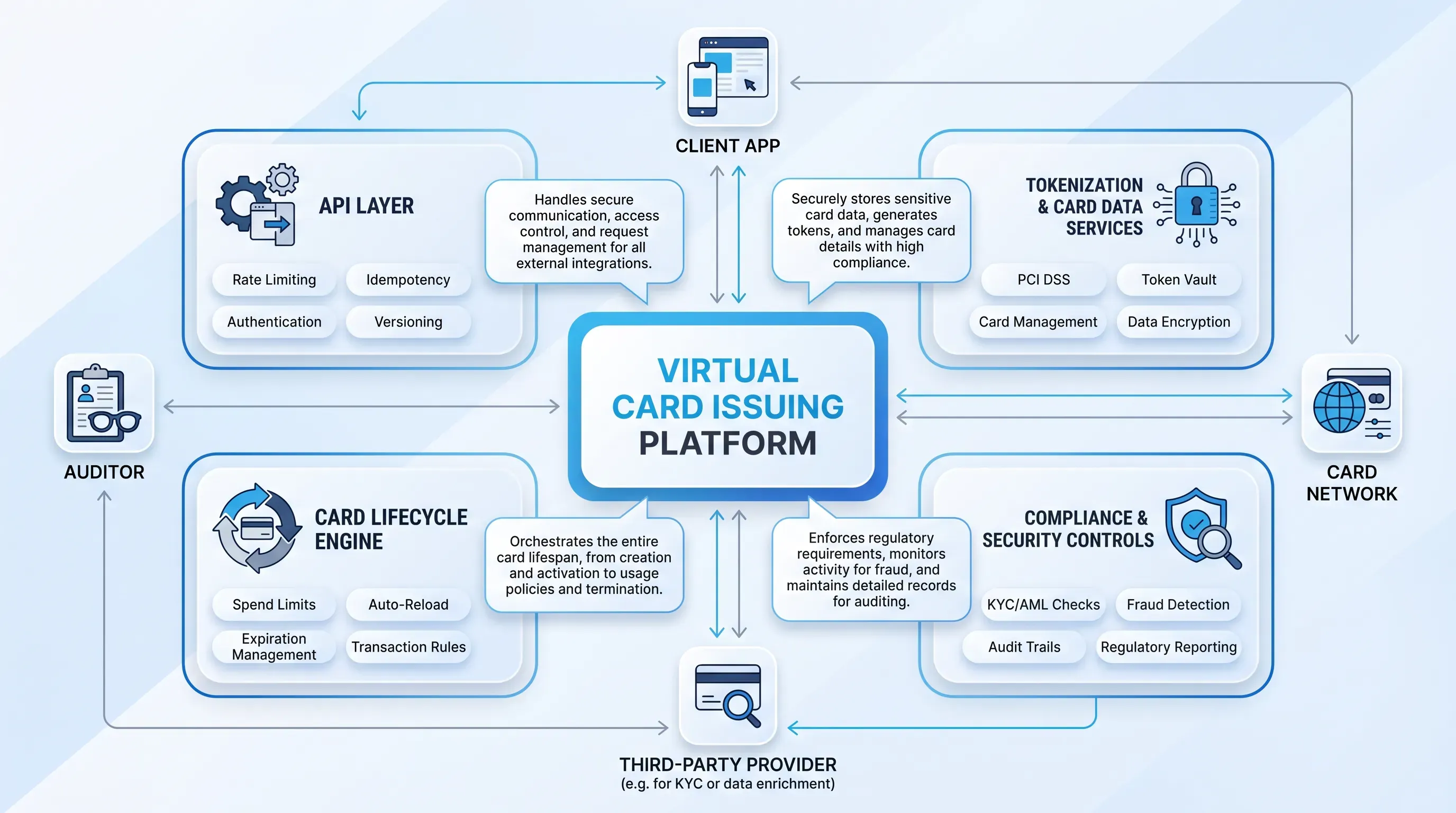

Security and compliance controls

Security on a virtual card issuing platform is layered, because no single control is enough on its own. Encryption protects data in transit and at rest, so even a captured packet or a stolen disk yields nothing usable. Access controls limit who and what can reach the cardholder data environment, and each service touches only the data it needs. The two work together, since encryption without tight access control still leaves keys exposed to anyone inside the perimeter.

The tokenization vault depends on secure key management, and this is where hardware earns its keep. A Hardware Security Module (HSM) is a tamper-resistant physical device that generates and stores cryptographic keys; it also manages key operations inside the device so the keys are never exposed externally. Futurex HSMs, for example, are FIPS 140-2 Level 3 and PCI HSM validated and handle key lifecycle management for payment systems. Keys that protect the vault rotate and expire, while certified hardware keeps them locked away from application memory.

All of this sits under the Payment Card Industry Data Security Standard (PCI DSS), which any organization has to meet when it processes cardholder data or handles its storage and transmission. Audit logging and continuous monitoring serve both security and the regulation at once, because the same records that let you investigate an incident also prove to an assessor that controls are working. Treat security as a one-time setup and it decays. The platforms that hold up treat it as a practice in which key rotation and access reviews are routine work, while log monitoring continues after launch.

Fraud detection and controls

Fraud detection runs in real time because the decision has to be made before the authorization clears. Global card fraud losses reached $33.41 billion in 2024 according to the Nilson Report, which is the scale of the problem these systems exist to contain. The virtual card issuing platform scores each authorization request as it arrives and decides whether to approve or decline it, with flagged cases routed for review.

The scoring combines a few approaches that each catch different things. Rule-based controls handle the clear-cut cases, such as a card used outside its approved merchant category. Velocity checks watch for patterns over time, like a sudden burst of authorizations on a card that normally sees one a week. Machine learning models score the gray areas by assigning a risk number from many signals at once. Visa's Advanced Authorization, in production since 1993, scores every transaction against more than 500 risk attributes in under a millisecond, which shows how tight the latency budget is and how much can still be evaluated inside it.

That latency budget is the hard constraint. A card authorization on VisaNet routes to the issuer in roughly 150 milliseconds, and the fraud decision has to fit inside that window alongside everything else the platform is doing. So the models are tuned to score fast, and the rules execute first because they are cheap. Configurability is what makes the system usable. A business sets its own thresholds for how aggressively to decline borderline transactions, which lets it balance fraud prevention against the cost of blocking legitimate spending. Set the dial too tight and you decline good customers. Too loose and losses climb.

Scaling for high transaction volume

Scaling a virtual card issuing platform means handling more cards issued and more transactions processed without authorization times creeping up. The work splits into stateless and stateful parts, and they scale differently. The API and authorization services are largely stateless, so horizontal scaling handles them by placing more identical instances behind a load balancer as traffic grows. The database is harder.

Database partitioning, or sharding, divides a large dataset into smaller pieces stored across separate servers so that no single server becomes a bottleneck. The shard key matters enormously, because a poorly chosen key forces expensive re-sharding later. Caching sits in front of the hot reads and keeps frequently accessed card and balance data in memory so an authorization doesn't wait on disk. Authorization is the latency-critical path, so the architecture is shaped around keeping that path short even as the data behind it multiplies.

Staying online through failures is its own requirement. High availability on a virtual card issuing platform comes from redundancy across multiple instances and availability zones, so the loss of one node or one data center doesn't take the system down. CockroachDB, for instance, distributes and rebalances data automatically as payment volume grows while preserving transactional guarantees, which removes the manual sharding work that otherwise grows more painful with every scale-up.

None of this comes free, and the trade-offs are real:

-

Strong consistency across distributed nodes costs latency, while relaxing it improves speed at the risk of stale reads

-

Redundancy and extra capacity raise infrastructure cost, which has to be weighed against the cost of downtime during a peak season

The right balance depends on the program. A platform processing prepaid disbursements tolerates different trade-offs than one running corporate travel cards at month-end peaks.

Final thoughts

On a virtual card issuing platform, architecture and security belong to one system, with scalability changing how that system behaves under load. The API layer is only as trustworthy as the tokenization vault behind it, while fraud controls work inside the latency the scaling design preserves and compliance depends on disciplined key management and access controls as volume grows. Thoughtful component design pays off most when a program scales, because the weak link is the one that breaks first under load.

When you evaluate or build one of these platforms, look hard at how tokenization reduces PCI scope and how the lifecycle engine enforces controls at authorization time, then test how the system stays available during failures. EGS builds resilient fintech infrastructure for exactly these demands. To see how a virtual card issuing platform can fit your program, reach out to our team for a consultation.