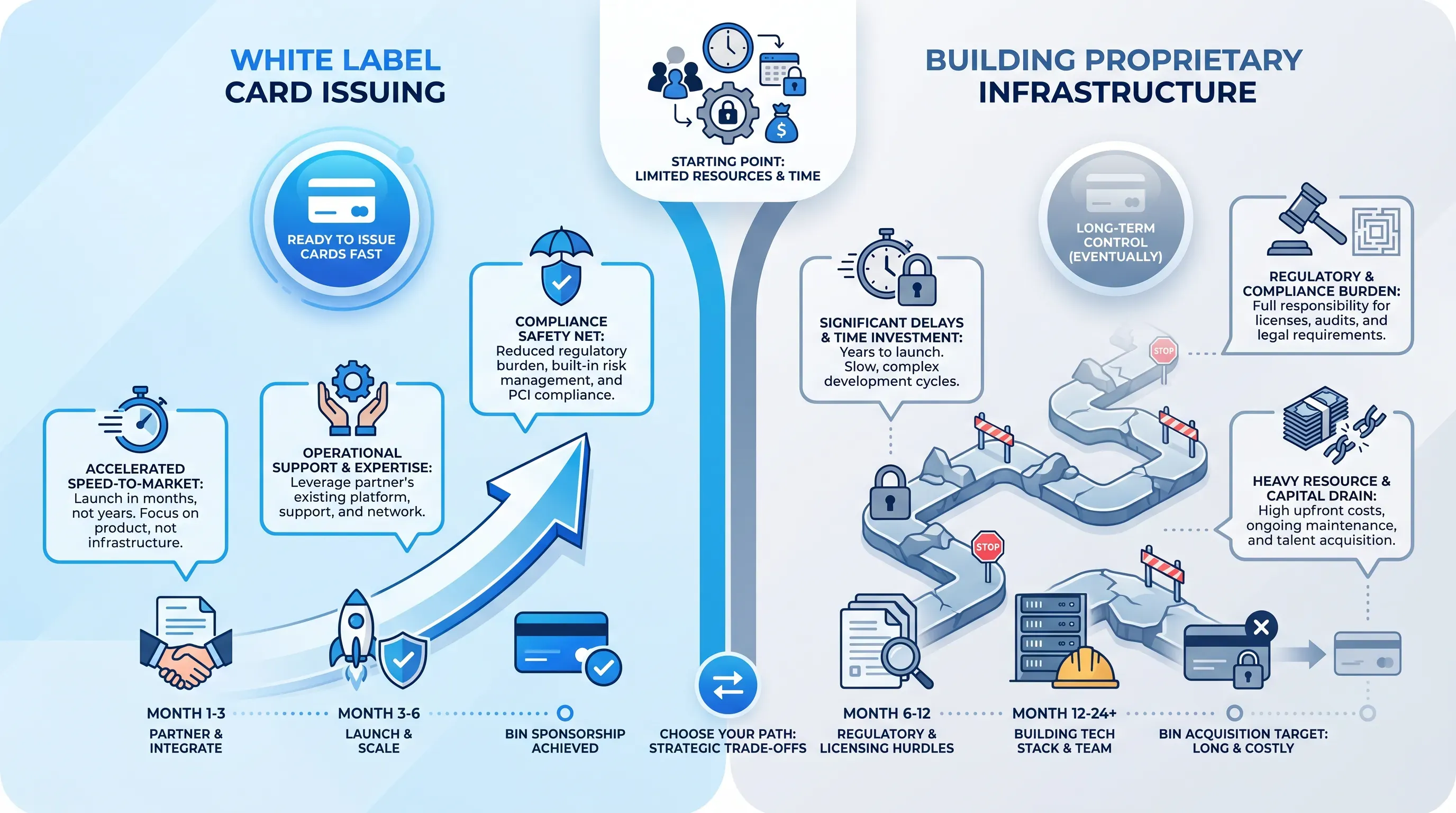

Speed to market matters most

Getting your own BIN through a sponsor bank takes time. Wallester puts the timeline at 3 to 6 months for a BIN alone, with more time required to launch the actual product. Galileo, the issuer processor SoFi acquired in 2020, says obtaining BIN sponsorship done independently can be a 6+ month process, while doing it through a market-tested partner can take as little as two months. Turnkey issuing solutions collapse that further because the provider already holds the BIN and the scheme certifications behind the processor integration.

For a team chasing a pilot customer or a Series A milestone, that gap is the difference between shipping and slipping. The trade-off is real. You accept the provider's product constraints, from its fee schedule to its supported card types, in exchange for time. That's a deal worth making when the launch window is the binding constraint.

Cards are a feature inside the product

For a Human Resources platform that issues a benefits card, or a rewards app that hands out a cashback card, the card is a distribution mechanism inside the product. Owning issuing infrastructure adds operational cost and engineering load while expanding audit exposure without changing what makes the company valuable. White label card platforms absorb that load and let the team focus on the actual differentiator, whether that's payroll or loyalty mechanics tied to employee experience.

Vertical Software-as-a-Service (SaaS) companies fit this pattern cleanly. The card is one feature among many. Building it from scratch instead of using white label card issuing would distract a small product team for a year and yield a card that looks identical to a licensed one.

Limited compliance and risk capacity

White label card platforms absorb a large share of the regulatory burden: scheme rule compliance, Payment Card Industry Data Security Standard (PCI DSS) certification, BIN sponsorship maintenance, and dispute resolution against network deadlines. For an early-stage team without a dedicated compliance officer, that's a meaningful safety net.

SDK.finance breaks down the split this way: under a sponsorship model the BIN sponsor ensures compliance while the fintech focuses on branding and product features that shape the customer experience. The chance of a launch-blocking audit finding drops because the regulated entity has done this dozens of times before. Your team learns compliance through work with the provider before audits test that knowledge.

Uncertain product-market fit

If the card program is still a hypothesis, white label card issuing is the cheapest way to test it. You're buying optionality. If the program works, you scale on the same infrastructure. If it doesn't, you shut it down without writing off a multi-year platform build. Early-stage teams using white label card platforms can pivot card types and target segments in weeks while staying on the same processor stack.

This matters because most card programs don't ship the right product on the first try. Treating the first version as a test, not a commitment, is what white label card issuing makes possible.

When building your own makes more sense

Flip the lens. Once a card program is the core revenue engine and the volume is real, provider fees start to bite. Interchange splits and platform minimums add up with each per-authorization charge. At scale, the unit economics of owning the processor relationship and negotiating directly with the networks on your own BIN can swing margin by hundreds of basis points.

The signals that point toward in-house build:

-

Volume is large enough that processor fees exceed what an internal team would cost to run.

-

The product needs features the provider can't ship on your timeline, such as a novel authorization model or exotic settlement currency support, with proprietary fraud logic handled in-house.

-

The card program is a strategic moat, not a side feature, and competitors are catching up because they're on the same shared infrastructure.

-

Regulators or partners require direct control over data and risk decisions that affect settlement and that a third party currently mediates.

The commitment is heavy. Marqeta, the modern card issuing platform that powers Block and Uber alongside DoorDash, reported Net Revenue of $507 million on $291 billion in total processing volume for 2024. That scale is what owning the stack looks like from the provider side. To replicate even a fraction of it internally, you need a compliance team, a network relations function, 24/7 operations, and engineers who understand ISO 8583 messaging. Galileo, after SoFi's $1.2 billion acquisition in April 2020, now powers 168 million accounts. Those numbers exist because building issuer processing well takes a decade.

For most companies, building in-house only makes sense once card volume is the primary lever for enterprise value. Below that line, you're paying a tax for distraction.