Real-time debit issuance explained

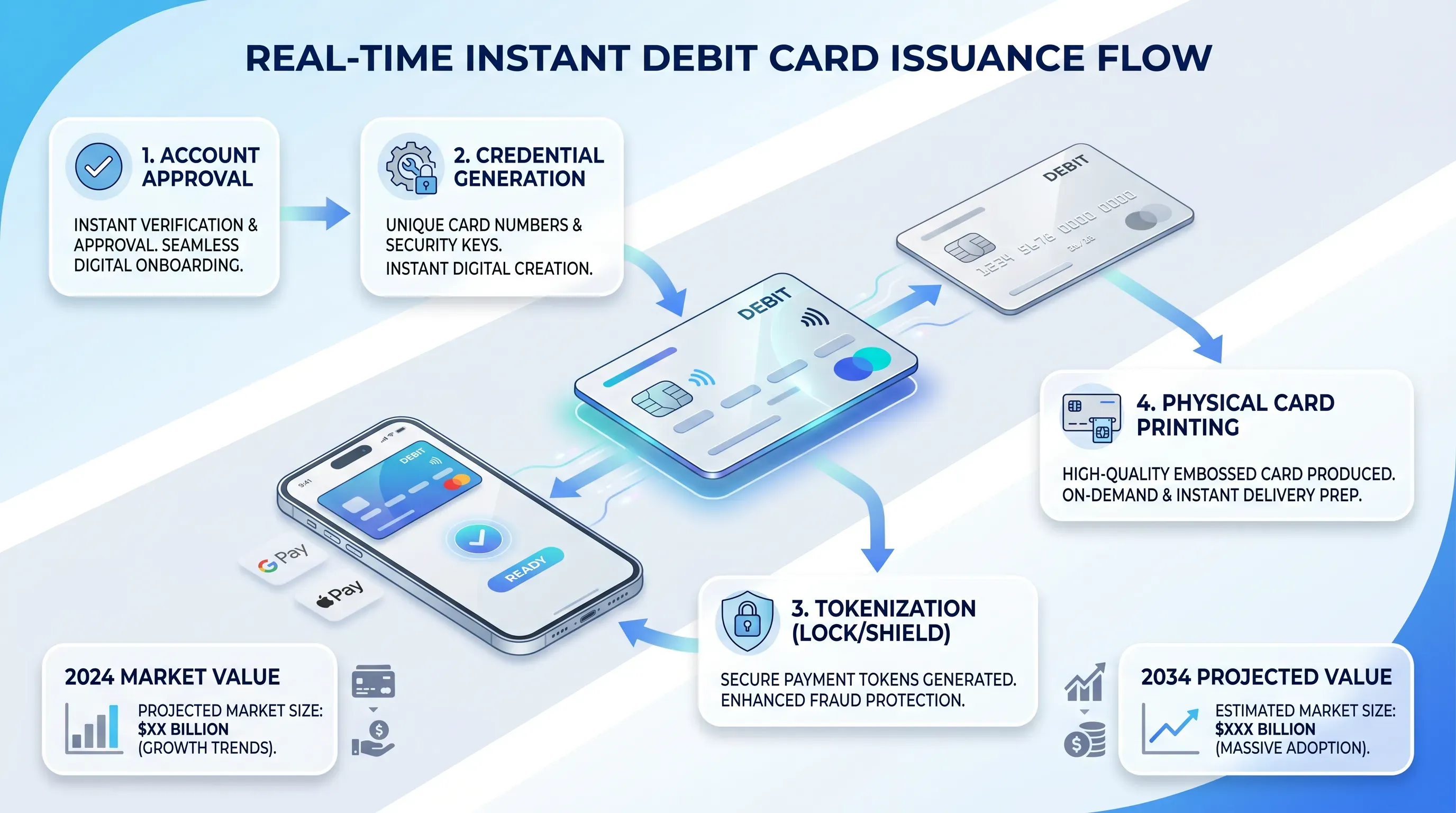

Real-time debit issuance is what produces those working credentials the instant an account clears approval. Three parties do the work behind the scenes. The issuer holds the account relationship, while the card network assigns a number from its range and the processor connects the two so the card can authorize transactions right away.

When those systems agree that your application passed, real-time debit issuance generates the full set of details that any card needs to function. You get a primary account number with its expiry date and security code, all valid from the first second. Because the credentials are live on the network, the digital card works for an online checkout or an in-store tap without anything physical changing hands.

This is the part that feels like magic to a customer and like plumbing to an engineer. Real-time debit issuance mints the actual card, which is why the number you spend with today is the number you keep.

Pushing cards to digital wallets

A fresh card number is only useful if you can spend it, so the next step is instant card provisioning into a wallet. The newly created card is pushed directly into a digital wallet or the issuer's own banking app. Checkout.com describes this as push provisioning, where the issuer adds the card to the wallet directly for the customer.

This step is what lets someone tap to pay at a register without ever touching plastic. Tokenization replaces your real card number with a secure token, and Google's developer documentation explains that Google Pay stores a device token called a DPAN that gets passed to the terminal in place of the actual number. The same logic runs Apple Pay, where the real details are never exposed.

Instant card provisioning completes the path from approval to first purchase. Once the token sits in the wallet, the customer is one tap away from spending. The whole sequence, from a green light on the application to a working tap-to-pay card, runs in seconds.

Linking to the physical card

Digital-first issuance still supports plastic. A physical card can still be ordered and mailed while the digital version is already in active use. The same account and card number carry over, so when the plastic lands in the mailbox, there's no new activation drama and no break in service.

Some issuers skip the mail entirely with instant card provisioning at the branch and print a personalized card on demand while you wait. Juniper Research notes that modern card programs support instant and personalized issuance of physical cards alongside virtual ones. Either way, the customer never feels a seam. The digital card covers the present, and the physical card slots in behind it without resetting anything.

The customer experience step by step

From the customer's side, the journey is short and almost entirely on a phone.

Here is the typical sequence:

-

Submit the application with identity details and any required funding.

-

Pass identity verification and receive account approval in under a minute.

-

Real-time debit issuance generates the live card number with its expiry and security code.

-

The card is added to a digital wallet through instant card provisioning.

-

Tap to pay in a store or use the card details to check out online.

What used to take a week now fits inside a single session. The approval and the first purchase can happen on the same screen, in the same few minutes. Speed matters at every step, and the wallet hand-off is where instant card provisioning turns an approved account into spending power. By the time most people would have finished the old paperwork, a customer here has already bought something.

Benefits for customers and businesses

Instant debit cards pay off on both sides of the counter. Customers get speed and convenience, while issuers get engagement and retention. The subsections below separate the two audiences so the value is clear for each.