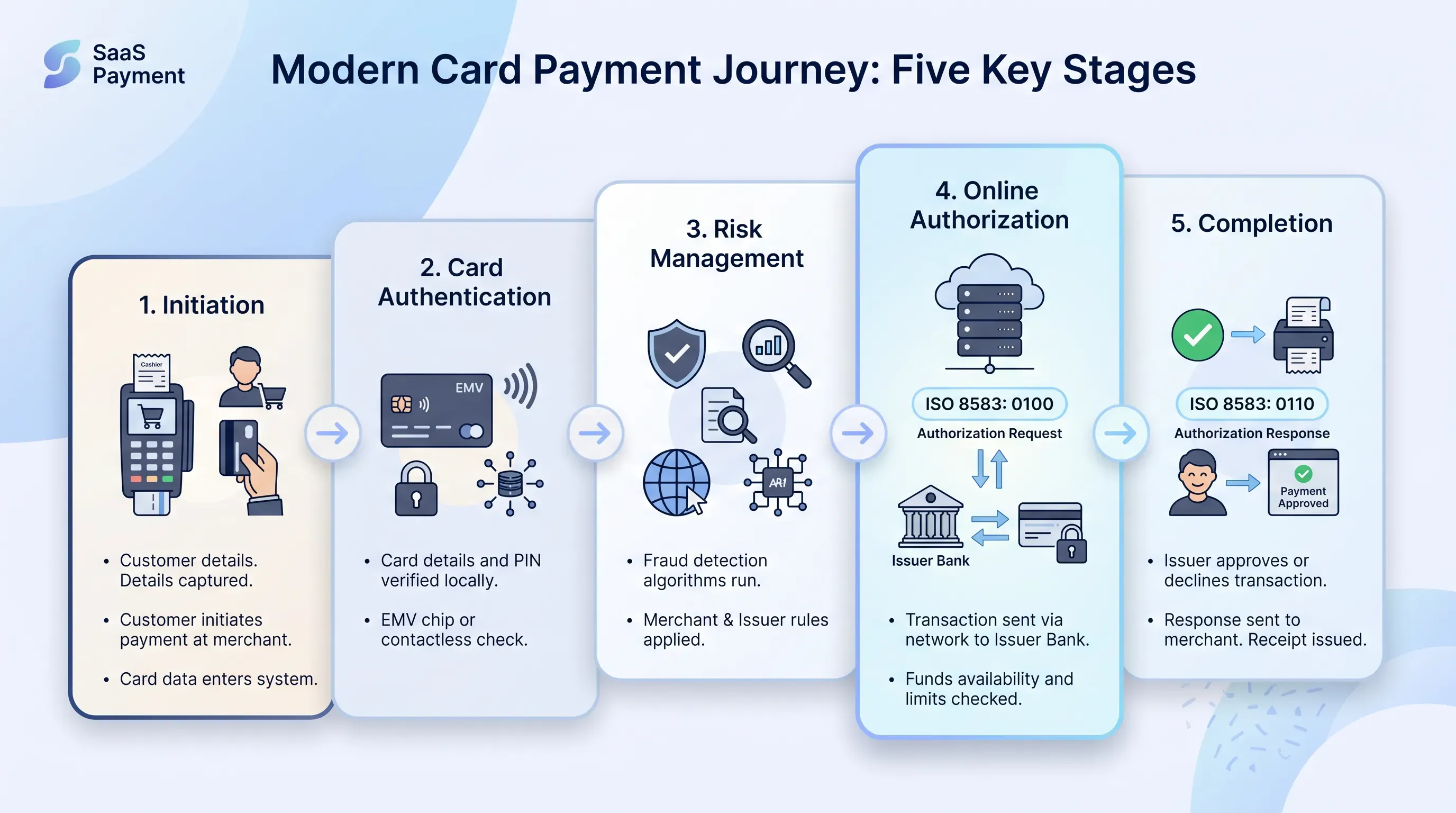

What happens after a customer taps their card

Now the switch integration layer in POS transaction software assembles the request. It builds an ISO 8583 0100 message from the card data and processing code, with the amount and timestamp included, and the bitmap flags exactly which fields are present before the request moves through the switch toward the card network and the issuing bank. The issuer checks the account and available balance against its fraud rules, then sends back a 0110 authorization response with an approval or decline code.

The response travels back the way it came. The switch layer parses the 0110, and the transaction processing layer records the result with the final EMV cryptogram before control returns to the UI, which prints the receipt and tells the customer they're done. In real-time POS terminal software development, one tap sends two ISO 8583 messages across the planet and back through the stack, all inside the window before a customer starts to wonder if something broke.

Latency budgets and offline modes

That window is the hard constraint behind everything. For card payments the round-trip authorization takes one to three seconds under normal conditions, and push past five and you start losing customers. So every layer operates inside a tight budget, and the fraud check alone must return in under 100 milliseconds at the 99th percentile. Tail latency is what matters, because the spike during peak traffic is exactly when the timeout hurts.

Then the connection drops. A terminal that simply fails here is useless in real-world payment terminal systems, so store-and-forward logic exists to keep the lane moving. When the switch is unreachable, the terminal authorizes locally within configured risk limits, then queues the transaction securely until it can sync.

A sound offline mode does the following:

-

Authorizes within preset risk limits after an amount check against a floor limit and a Bank Identification Number (BIN) screen

-

Encrypts each approved transaction for a secure local queue, then forwards the batch for settlement the moment connectivity returns

Offline mode is a deliberate engineering feature with liability attached. The trade-offs are concrete. Stored transactions carry time limits, because the longer one sits, the higher the chargeback exposure if the card turns out to be bad. Duplicate detection has to run so a transaction queued offline isn't also sent online, and reconciliation must run on every sync to confirm that what the terminal stored matches what the backend settled. The EMV specification leans on the same idea and requires a card to go online once the cumulative offline amount or the count of consecutive offline transactions crosses the issuer's limit. Decide those thresholds with your acquirer, because they are choosing how much risk you absorb.

Security and PCI PTS compliance

Security in real-time POS terminal software development is architectural from the first line of code. The governing standard for the device is PCI PIN Transaction Security (PTS) Point of Interaction (POI), which sets the requirements for secure PIN entry and cardholder data encryption, with physical tamper protection and cryptographic key handling inside the same control model. The current v7.0 standard introduced 59 requirement changes for biometric interfaces and open software platforms, with wireless connectivity also inside its scope. Get this wrong and the device fails deployment, which is why it shapes the build.

The protections interlock as one system. Secure boot establishes a hardware root of trust so the device runs only signed firmware from the first instruction, and tamper detection responds to physical attack by zeroizing keys. Adyen's PCI PTS 6 work describes mandatory three-year firmware revalidation alongside secure boot, and runtime integrity checks make the certification continuous. These hardware guarantees are what let the higher layers trust the data they handle.

Above the device, two techniques shrink your exposure. Point-to-point encryption (P2PE) encrypts card data the instant the card is tapped or inserted, before it reaches any of your systems, and a PCI-validated solution can lower PCI scope by up to 90%. Tokenization then replaces the stored account number with a meaningless surrogate, so a breach yields nothing usable. The two work as a pair: P2PE keeps clear-text data out of the environment, and tokenization keeps it out of storage. Underneath both sits key management, which is the quiet thing that breaks programs when it's an afterthought. Keys must be generated and stored inside the secure boundary, with rotation governed there too, because a perfect encryption scheme with sloppy keys protects nothing.

Why end-to-end POS engineering wins

A terminal app on its own is half a solution in real-time POS terminal software development. The value lives in the whole chain, from the secure runtime on the device through switch integration to the backend that handles authorization routing and settlement. The transaction you followed earlier touched all of it, and a gap anywhere shows up as a failed payment or a reconciliation mess.

Fragmenting that chain across vendors is where projects stall. One vendor ships the terminal app while another owns the backend, and the ISO 8583 dialects don't line up at the seam. When a payment fails, that seam obscures ownership. The certification headaches compound because PCI PTS and EMV kernel approvals assume a coherent system. A single partner who owns both the terminal and the backend removes those seams and cuts time to market.

That is the position EGS takes as a payment terminal systems engineering partner: it owns the full path from the secure terminal runtime to the backend so the whole chain becomes one accountable build. If you're scoping a roadmap and want a clear read on what real-time POS terminal software development requires end to end, reach out to discuss your build.